Go | New | Find | Notify | Tools | Reply |

| Eschew Obfuscation |

Thanks but that is not an issue. We worked with a financial advisor and our retirement plan does not take Social Security into account. _____________________________________________________________________ “One of the common failings among honorable people is a failure to appreciate how thoroughly dishonorable some other people can be, and how dangerous it is to trust them.” – Thomas Sowell | |||

|

| Eschew Obfuscation |

One quibble and one add: quibble: My only add would be: If someone is offering you free money, take it. I'm thinking stuff like 401k matching. If your employer matches up to a certain percentage, it would be foolish not to take it. I was talking to a fellow whose employer offered 6% matching on 401k contributions, and he knew people who were not putting in 6%! Hello!? _____________________________________________________________________ “One of the common failings among honorable people is a failure to appreciate how thoroughly dishonorable some other people can be, and how dangerous it is to trust them.” – Thomas Sowell | |||

|

Member |

Risk Gambling Correction As long as the market goes up-all is good. If market goes done - there is the potential for a significant loss. There is no stock market insurance. I don't have that "sense of security" in the stock market. Im in the low risk pool-- 4-6%. | |||

|

| Lawyers, Guns and Money  |

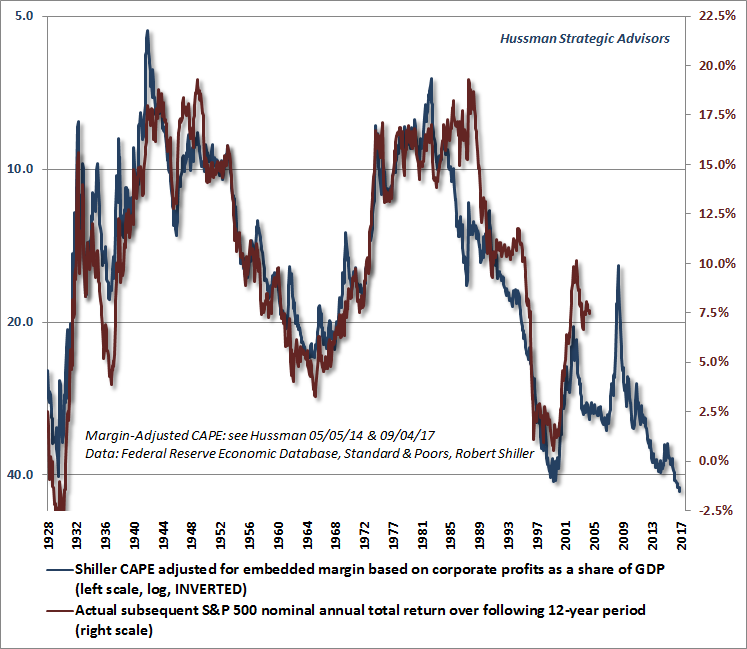

The case for lightening up your exposure to the stock market...: The Waiting Is The Hardest Part Man, what an awful stretch of events. When I penned last week's article on tragedy, little did I expect something as horrible as the Las Vegas massacre would immediately follow. And nearly lost in the headlines was the untimely passing of rock legend, Tom Petty, one of my all-time favorite musicians. Sure can't wait for this week to be over...  In memory of Tom, I've been listening to a lot of his and the Heartbreakers' best hits. The lyrics to one song in particular, The Waiting, well-captures an important message today's investors should take to heart: The waiting is the hardest part Don't let it kill you baby, don't let it get to you Those waiting for the financial markets to experience some sort (any sort!) of pullback have been waiting a long, looong time. How long? It has been over 100 months (more than 8.5 years) since the current bull market began in April of 2009 It has been 15 months since the last (and very brief) drop of 5% in the S&P 500 This past September saw record low volatility, including a stretch now claimed to be “the most peaceful days in the history of the markets” Since last year's presidential election, at which point the markets were already considered dangerously overvalued, the Dow Jones Industrial Average is up over 20% As of this article's publishing, the Dow, the S&P and the NASDAQ are all trading at record highs Or, to put it visually:  The stock market is now 70% higher than it was at the previous bubble peak immediately preceding the 2008 Great Financial Crisis. Reflect for a moment how painful the crash from Oct 2008-March 2009 was. How much more painful will a crash from today's much dizzier heights be? Prudent investors have asked themselves that very same question as the markets have become increasingly overvalued over the past 8+ years. Many of them -- myself included -- concluded that the future risks greatly outweigh the prospect of future returns, and pulled much of their capital out of the markets onto the sidelines. And since doing so, many of them -- again, myself included -- have watched prices climb higher and still higher again. It's understandable to feel great frustration both at the irrationality of today's market prices and at the emotional sting of missing out on the gains they've been delivering to those who have blithely remained long. But it's very important to remember we've been here before many times throughout history (and pretty recently when reflecting back on the Tech and Housing bubbles). While today's levels are at a historic extreme, markets have always swung from periods of overvaluation to undervaluation -- and then back again. During the peaking process, the siren call to join the party is incredibly hard to resist. Waiting out the irrational exuberance leading up to a market top is painful. Profitable returns are everywhere. How can you turn down making such easy money? As Tom Petty sympathized: The waiting is the hardest part. But the disciplined few who can wait out the mania of a bubble become the big victors once it pops. Capital that they've held in reserve as "dry powder" can suddenly purchase assets at half (or even less) the prices they commanded just months earlier. This has happened in (recent) living memory: the S&P 500 lost 50% of its value between its 2007 high and its 2009 low. So the big question to ask yourself is: Do you have the fortitude to endure the wait? I ask myself that a lot. Because "doing nothing" is hard. Especially when listening to the gloating of those enjoying the returns on their portfolios, unconcerned and uninterested in any warnings the fundamentals might be waving. But I draw strength to remain committed in my course from several areas. One of them involves an argument made by Peak Prosperity's resident technical analyst, Davefairtex, who posits that a successful investing strategy can involve just a single move every half-decade or so: In my opinion, the market has always been a skimming machine that funnels money and wealth from the many into the voracious maws of the few. Here's the intro of a book written in 1940. Where are the Customer's Yachts? -- Fred Schwed, Jr, 1940. Once in the dear dead days beyond recall, an out-of-town visitor was being shown the wonders of the New York financial district. When the party arrived at the Battery, one of his guides indicated some handsome ships riding at anchor. He said, “Look, those are the bankers’ and brokers’ yachts.” “Where are the customers’ yachts?” asked the naïve visitor. --Ancient story Hussman offers a methodology to keep "the customers" from repeatedly getting their pockets picked. He uses a very long term "10 year expected returns" calculation to show if the market is expensive or cheap. Right now: expected return for the next 10 years is about 0%. Message to "the customers": don't freaking buy! As a charter member of the "customer" group, you will need to stay away from the market for many years if you use this metric. As a reward, you won't suffer the 40% drawdowns and sell at the bottom, and you will have the opportunity to buy low - right down there at the bottom when fear is at maximum. Everyone will think you are stupid for years at a time. You will miss out on years of ponzi and have to endure years of worry. You will not have very much company to make yourself feel better. Good news is, you'll only need to make a decision once every 4-6 years. Can you do it? For those curious to see for themselves what the Hussman chart Dave refers to looks like, here's the most recent version, which now predicts a negative total average return for the next 12 years:  I like Dave's direct challenge of "Can you do it?". Do you have the emotional fortitude to resist the allure of easy returns when the market is delivering them week in and week out? Can you resist the very human urge to try to "beat the market" in any given year, and instead simply wait for the obvious periods of undervaluation that indicators like Hussman's chart above will identify for you? And if you can, will you have the iron stomach to deploy your capital at those times, when everyone else is decrying their losses and claiming the market is a death trap? I aspire to answer "Yes!" to each of those questions. I think many of you reading this do so, too, which is why I'm sharing all this. I find it helps tremendously to be reminded of the fundamental reasons why we are choosing safety today in order to enjoy opportunity tomorrow. And to know that you're not alone in your stoic discipline. Also, there *are* valuable actions we can take today while we wait for the market to re-adjust. One is to take good care of your capital while you're keeping it on the sidelines. I've written in the past about the insultingly-low interest rates (e.g., 0.06%) offered by savings accounts at most banks these days. There are ways to get 15-20x higher return on your cash savings with no loss of safety or lengthy tie-ups. Ask your professional financial advisor for a range of such options -- or schedule a free discussion with our endorsed advisor, who will detail the solutions they recommend (including several of which you can do on your own). Another is to educate yourself on which indicators (like Hussman's expected returns chart above) to track to monitor where we are in the boom/bust timeline. We discussed a number of those in last month's excellent Dangerous Markets webinar with Grant Williams and Lance Roberts (if you haven't already watched it, you really should). But we're really going to dig deep into which key data to monitor at our upcoming Peak Prosperity summit in New Orleans on October 27th. Join us there if you can. And last, remember that besides Financial Capital (aka 'money'), there are seven other Forms Of Capital that require an equal degree of your attention. Growing your wealth balance in each one of them is every bit as important as your financial net worth. Tom was right: The waiting is the hardest part. Best we use that time as wisely as we can. http://www.zerohedge.com/news/...waiting-hardest-part "Some things are apparent. Where government moves in, community retreats, civil society disintegrates and our ability to control our own destiny atrophies. The result is: families under siege; war in the streets; unapologetic expropriation of property; the precipitous decline of the rule of law; the rapid rise of corruption; the loss of civility and the triumph of deceit. The result is a debased, debauched culture which finds moral depravity entertaining and virtue contemptible." -- Justice Janice Rogers Brown "The United States government is the largest criminal enterprise on earth." -rduckwor | |||

|

eh-TEE-oh-clez |

My 401k managed by John Hancock does not seem to be doing fantastic. 4.6% or so. I'm 35, and I have it set for retirement in like 2050, so that's a little disappointing. I have money in a Wealthfront account, and that's doing better, 10% money-weighted. But I have money in a Motif account that is doing 78.5% YTD. | |||

|

| Inject yourself! |

16.7% last year and 5% for 10 years. I've made some changes based on my advisors advice, so it will take a bit to even up I think. Mid 30's with a desire to retire at 55-57. There is not an encouraging amount in the Vanguard 401, but it's increasing. I haven't taken a raise home for a while now, it goes into the 401. I'm trying to get to the full amount allowed per year, and I'm 2/3rds there or close. I'm working toward the amount suggested by my advisor to invest with Edward Jones. I'm not super comfortable with my risk level, but at the level I'd be comfortable at, it wouldn't make hardly any money. I'm not counting SS and only half of my other potential income, which puts me ok to retire when I want. We're also not counting on the wife's retirement, planning to retire only on my retirement and have hers be the extra or fun money. Balancing fun and retirement is so very adultish, ugh. Do not send me to a heaven where there are no dogs. Step Up or Stand Aside: Support the Troops ! Expectations are premeditated disappointments. | |||

|

| stupid beyond all belief |

Consider buying Snap Inc for FB. It is the GE of our time. What man is a man that does not make the world better. -Balian of Ibelin Only boring people get bored. - Ruth Burke | |||

|

Member |

Aren't you glad you checked? The danger of baobabs is so little recognized. | |||

|

| Lawyers, Guns and Money |

"Some things are apparent. Where government moves in, community retreats, civil society disintegrates and our ability to control our own destiny atrophies. The result is: families under siege; war in the streets; unapologetic expropriation of property; the precipitous decline of the rule of law; the rapid rise of corruption; the loss of civility and the triumph of deceit. The result is a debased, debauched culture which finds moral depravity entertaining and virtue contemptible." -- Justice Janice Rogers Brown "The United States government is the largest criminal enterprise on earth." -rduckwor | |||

|

| Lawyers, Guns and Money |

Index Change YTD % DJIA 19.2 Nasdaq 28.0 S&P 500 16.2 Russell 2000 11.9 "Some things are apparent. Where government moves in, community retreats, civil society disintegrates and our ability to control our own destiny atrophies. The result is: families under siege; war in the streets; unapologetic expropriation of property; the precipitous decline of the rule of law; the rapid rise of corruption; the loss of civility and the triumph of deceit. The result is a debased, debauched culture which finds moral depravity entertaining and virtue contemptible." -- Justice Janice Rogers Brown "The United States government is the largest criminal enterprise on earth." -rduckwor | |||

|

goodheart |

This is why I haven't rolled over from previous employer's 401k to IRA, the latter doesn't offer Primecap Admiral. I have a very long time horizon even though retired, because we are fortunate enough not to have to draw on the capital. Plan is to re-invest almost MRD's. _________________________ “Good intentions will always be pleaded for every assumption of authority. It is hardly too strong to say that the Constitution was made to guard the people against the dangers of good intentions. There are men in all ages who mean to govern well, but they mean to govern. They promise to be good masters, but they mean to be masters. –Daniel Webster (1782-1852)" | |||

|

| Get busy living or get busy dying!  |

Buy and Hold (which most people do in their retirement accounts) is for losers. Why do people stay in a falling market??????????? In looking at the chart above, what if you could get out of the market after the index falls about 7-10% and then buy back in after the market bottoms and starts climbing? The answer is - Your profits will be huge!!!!! An example of what I describe above is: www.smartmarkettiming.com, it has made 30% each year 2016 and 2017. | |||

|

| Member |

Much better than they will be in Q2. | |||

|

| goodheart |

The argument I've read against "timing the market" is that no one can predict the bottom, and historically, rebounds of the market have appeared in a very short period of time; so if you weren't in the market at the bottom you lose the gains in the rebound. _________________________ “Good intentions will always be pleaded for every assumption of authority. It is hardly too strong to say that the Constitution was made to guard the people against the dangers of good intentions. There are men in all ages who mean to govern well, but they mean to govern. They promise to be good masters, but they mean to be masters. –Daniel Webster (1782-1852)" | |||

|

| Member |

Im probably around +20%. Except for that Chipotle stock which I bought a week before the outbreak occurred. Now its down 40%. | |||

|

| Get busy living or get busy dying! |

If you look at missing the big fall, you don't have to time the market perfectly. If you can avoid a 33% loss (like in 2008) your 50% rise is off a much higher base value. Remember, if you lose 33%, you have to have a 50% rise TO GET BACK TO WHERE YOU WERE! | |||

|

Yokel |

One account 14.41% over 12 months 67.84% over 5 years. Other account 17.50% over 12 months, 7.2% over 5 years.This one is mostly Oil Company Stock with good dividends. I have been drawing the dividends the last 5 quarters. Beware the man who only has one gun. He probably knows how to use it! - John Steinbeck | |||

|

His Royal Hiney |

My benchmark is from April 31 of this year just because of what I did with my funds. Over that 7 months, it grew 12.8%. If I do a rough extrapolation, that's 22% annual rate. A good portion of that rate was by my wife when she had been managing our 401ks because I was too busy. When I was doing it, I subscribed to several expensive services like Money Market, Morningstar, Valueline, Cramer's, and Upgrader. But I still managed to lose money. She started from no knowledge, just read Money Magazine and watched financial shows and she did very well. For example, she bought Amazon on Sep 2016 at $800 and bought more in March this year at $850 and the price is $1,186 now. I know that's something I wouldn't have done. She also bought VISA when it had an IPO in 2008 and it's 650% from that time. I also see a holdover from when I was managing the portfolio - Cano Petroleum that I bought 600 shares at $8.52 and it's worth zip now. Schwab won't take it out of my statements for some reason even after I asked. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| Member |

Pretty dang good this year. MAGA. ----------------------------------- Proverbs 27:17 - As iron sharpens iron, so one man sharpens another. | |||

|

| Lawyers, Guns and Money |

The current bull run is comparable to the one in the 1950s in duration and total gain.  "Some things are apparent. Where government moves in, community retreats, civil society disintegrates and our ability to control our own destiny atrophies. The result is: families under siege; war in the streets; unapologetic expropriation of property; the precipitous decline of the rule of law; the rapid rise of corruption; the loss of civility and the triumph of deceit. The result is a debased, debauched culture which finds moral depravity entertaining and virtue contemptible." -- Justice Janice Rogers Brown "The United States government is the largest criminal enterprise on earth." -rduckwor | |||

|

| Powered by Social Strata | Page 1 2 3 4 5 6 7 ... 12 |

| Please Wait. Your request is being processed... |

© SIGforum 2026