Go | New | Find | Notify | Tools | Reply |

| Optimistic Cynic |

Did a thought experiment once, "How much money do I need to live the lifestyle I want?" Came up with the sum of $100 trillion. Figured it might be easier to moderate my expectations. I think the latter is the answer, you can retire on any amount of money if you can manage yourself, it's not about managing the money. | |||

|

Fighting the good fight |

It seems you're ignoring returns altogether with your calculation. I would certainly hope you wouldn't just park that $2M in a checking account and withdraw $80k/year until it's totally gone in 25 years. Instead, this "4% Rule" envisions investing that $2M in ultra-safe investments like bonds/TIPS/money market/CDs/etc., and earning 3%-5% back on it annually, thus causing their balance to remain relatively flat throughout retirement despite withdrawing that 4%/year. | |||

|

Member |

What are the assumptions of the 4% rule for equity and bond investments.? For the $2M example above, assuming it's parked in a 401K, what mix of equity and bond does it assume? What does it assume the average return to be for the equity? For the bond? "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Member |

So the 4% rule only assumes that, wherever the money is parked, it's returning at least 4%? And if so, then the fund will last indefinitely? And the principle is essentially untouched (pulled for emergencies or during economic shocks)? "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Fighting the good fight |

Correct. | |||

|

| Member |

In my opinion the two major issues are debt and medical expenses. In the OP's case, wife will have 3 years before qualifying for MediCare, so medical insurance will be a concern during the interim (actually it will always be, but once we hit 65 Medicare is mandatory and serves in a primary role). If the OP's policy provides spousal coverage this could already be dealt with; otherwise OP may be shopping for a policy which will not be inexpensive for a 62-year old spouse. After MediCare enters the picture you will probably want to consider supplemental coverage to protect against potentially large co-pay and deductible requirements on MediCare alone. Debt can change the whole financial planning game. Mortgage, rent, and other significant recurring expenses must be covered by after-tax income before any other expenses can be considered. I have 100% VA medical coverage (disabled veteran), so my needs are provided for as well as can be achieved (no deductibles, no co-pays, no premiums). My wife was "down-sized" out of her career at age 57, so we had 8 years of private health insurance before she qualified for MediCare (well over $1000 per month). After 65 we added a good supplemental plan ($380 per month), thus saving a big chunk. We retired completely debt-free, home and everything paid off, so our budgeting is limited to recurring expenses like groceries, transportation, utilities, property taxes, insurance. Two Social Security benefits plus my VA disability compensation cover everything comfortably. We also have several retirement accounts and investment accounts. Now at age 73 we are dealing with the Required Minimum Distributions (RMD), drawing just enough to escape tax penalties on the qualified accounts (401, IRA, etc). We are able to continue saving and investing, as well as assisting 2 grown sons, 9 grandchildren, and 9 great-grandchildren without depleting the lifetime accumulations. A couple of trips or vacations per year are easily covered. Way too many variables to give a simple response to "how much is enough". In our case the balances continue to grow so we have few financial worries about the future. We also have a lifetime of living within our means and continually saving and investing, so perhaps more fiscal discipline than others who have always lived upside down in debt and relying on the next payday to cover last month's bills. The number for us was $1.3 million ($1.0M savings, investments, retirement funds plus $0.3M in real estate, etc). Now retired for 8.5 years with $1.3M balances and $0.45M real estate, etc. We are staying ahead of the game for now, but who knows what challenges the future will present. Continuing inflation, long-term care, downturns in the financial markets could change the game any time. Retired holster maker. Retired police chief. Formerly Sergeant, US Army Airborne Infantry, Pathfinders | |||

|

| Green grass and high tides  |

Konata, as far as a mix to reach a 4% return or there abouts is difficult to say. a 50/50 mix is not going to get that for you in todays market. If the market drops tradition thinking is the bonds will help and probably the 4% easily achievable. If you had a 75/25 mix yes in this market you could conceivably be considerably over the 4%. But if the market drops 15-20% you would most likely be in negative territory. You just have to do what makes you comfortable considering where you are at in your timeline. One thing you can try to do is if you determine you are more comfortable in a 50/50 mix or even 40/60 and your returns are treading water. You can take a small percentage of your portfolio and invest it in 75/25 or 80/20 mix and let it ride more for the long term. Hope that makes a bit of sense. And as far as the thread in general is concerned. You can only control what you can control. "Practice like you want to play in the game" | |||

|

| Partial dichotomy |

Don't forget inflation's effect. Passive income is a fine thing! Given a healthy retirement projection, also don't forget to include a little bit of growth to your portfolio. SIGforum: For all your needs! Imagine our influence if every gun owner in America was an NRA member! Click the box>>> | |||

|

Drill Here, Drill Now |

The 4% "rule" was from an economist's paper in 1994. He modeled modeled retirement withdrawal of 4.0% with an annual withdrawal increase of inflation (i.e. only year 1 was a 4.0% withdrawal and every subsequent year had inflation added), and the data model ended in the early 90s. However, you have to look at what's changed since the data set used in that model. Three examples: That's why many people are saying 3.33% to 3.5% for 30 years and the 4.0% is more like 25 years. The more sophisticated monte carlo modeling I mentioned earlier in the thread was eye opening for me when I varied how much money I spent annually and the effects on probability of success. Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| Fighting the good fight |

It doesn't require you to be in stocks at all (and the average retired person wouldn't/shouldn't be heavily invested in stocks to begin with). Even if you play it ultra-safe and are 100% in TIPS and US government bonds, the average annual return is over 4%. | |||

|

| If you see me running try to keep up  |

I am about 5 years away from retirement and I frequently read opinions from financial people on what is needed. I am seeing a trend in articles stating you can retire comfortably on less than a million, definitely a turn in advice from what has been stated in the past. It’s probably mainly due to the fact that most people will never achieve savings of a million, in fact, I doubt the majority of American even have an emergency fund saved up much less retirement savings. I predict there will be a lot of elderly in very poor financial shape when those in their teens and 20’s right now get to their 60’s and 70’s. They will depend on Uncle Sam to bail them out. | |||

|

| Fighting the good fight |

Cost of living is a major factor. People making broad generalizations like "a person in the US needs $2M to retire" are having to take into account the large number of folks living in super high COL areas like NYC/LA/etc. Whereas you don't need anywhere near $2M to retire to the rural South. Hell, the median household income in Arkansas (for example) is only around $50k.

It's not just those in their teens and 20s... I read an article a week or two ago stating that the median total retirement savings in the US for folks currently in their 40s is something like $45k! They're not going to be able to go from $45k to $1M in 10-20 years without stuffing a large percentage of their income into retirement savings. And if folks haven't already been doing that by their 40s, they're not likely able/willing to start now. | |||

|

| Green grass and high tides |

I am sure you are correct. But how many of those folks rent or have huge mortgage balances and have huge cc balances and many other debt responsibilities. I would venture to say the vast majority of these folks have little or no retirement. and never will. Not saying that people cannot live inexpensively in retirement. Many can and do.. "Practice like you want to play in the game" | |||

|

| Drill Here, Drill Now |

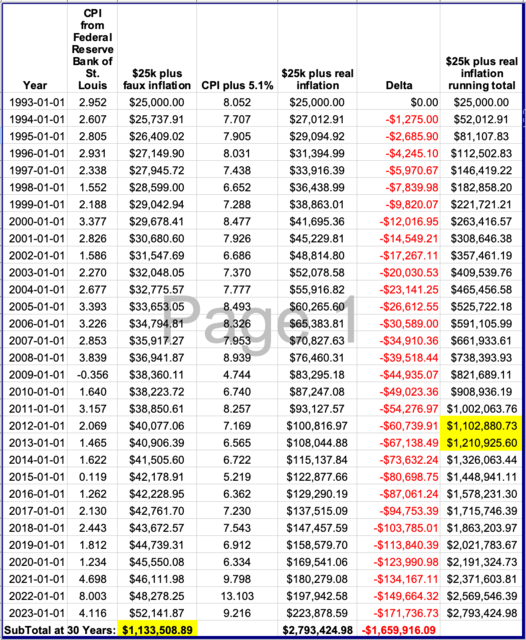

You're ignoring a key part which is inflation. I'll come back to portfolio at the end. Let me explain it a different way. The premise of the 4% rule is that you want to maintain the exact same lifestyle (i.e. every year you add inflation to previous year's withdrawal), but after the 4% rule paper was written the way inflation was calculated changed. Let's say that lifestyle in year zero is 25k more than income (e.g. pension, annuities, soc security, etc). Best I've been able to discern is that on average there is a 5.1% difference in real inflation. Here is what 30 years of most recent inflation looks like:  The column titled "$25k plus faux inflation" is the way the 4% rule assumes you're spending your money, but to actually maintain the exact same lifestyle is the column titled "$25k plus real inflation." There is an nearly $1.7 million difference in spending over 30 years to maintain the same lifestyle. To find the number of years that you maintain the same lifestyle you have to match the total at the bottom of "$25k plus faux inflation" to the same amount in column titled "$25k plus real inflation running total". I've highlighted in yellow when it matches. Based on that inflation information, you're faced with choices: Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| No More Mr. Nice Guy |

Depending on many assumptions, you can pull about 5-6% of your portfolio balance this year, then adjust for inflation each following year. That says you need about $2M in your portfolio to pull out $120k per year. Which is a very rough guesstimate. Social security might be half of your $10k income per month, so your portfolio might only need to be about $1M. It turns out there are specific months in the past when, if you retired that month, you ran out of money in less than 30 years, but the majority of months you would not have run out. So exactly when you retire is a gamble on the unknown, but generally the standard ideas are quite safe. The thing to watch out for is a big loss very early in retirement. Losing 40% of your portfolio in the first year is tough to recover from! We are using "guard rails" to modify our annual spend. We start with 5% of our portfolio on the day of retirement, and adjust annually for inflation. Then look at the Dec 31 portfolio value. If our new spend is more than 6% of our portfolio (meaning the portfolio dropped a lot), we reduce our spend by some. Conversely, if our spend is now less than 4% of our portfolio we increase our spend some, because our portfolio grew a lot and we can spend more. Note that your home equity is an asset. You can count some of that in your portfolio, keeping in mind it is an asset that will probably grow and which you can use in the future, but also consider you cannot easily or cheaply access it while living there. | |||

|

| Member |

Thanks! Helpful and makes sense. Approaching the end, I'm at 60/40. And now real inflation (ie - my weekly supermarket bill has almost doubled in the past 5 years) vs the gov faux-inflation is concerning me. Not sure how to handle that. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Member |

The info in the link, albeit rough and high level, is interesting. Quick scan of the list: 1. the gilded cage, as expected is perceived as one of the worst states. 2. FL, NV, TX, TN seem attractive 3. CO, GA, ID, IA, NC,OK, SC, SD, UT, WA, WV, WY are curious. I need some help and structure to disposition these. (local social/culture fit, weather, water, food (can I get the stuff I want), activities, medical, cost of living, home insurance, etc - basically, how well does the area specifically fit me and my likes/dislikes). "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| No More Mr. Nice Guy |

Yeah, you're good. Make a budget, stay within it, and you should be able to keep your current spend level. Typically as we get deeper into retirement our spending decreases, which further improves the odds of your plan succeeding. Taxes can be a big surprise, depending what kind of account your savings are in. Your fiduciary should be doing a lot of modeling and optimizing for taxes. e.g. it can make the most sense to pull from your 401k first even though you pay taxes now. Your Roth can grow tax free, and then your RMDs will be lower later. Some investments such as federal bonds are not taxed at the federal level (state taxes depend where you are) so it may be advantageous to hold them in your regular taxable account rather than 401k. SS and Medicare have some steep trigger points. Again, all this is stuff your fiduciary should be modeling for you, optimizing it for your specific situation. | |||

|

| Member |

Nuance but if I have a T-bill bond fund in my 401k, would this be subject to federal taxes? Is it only directly held T-bills that would be exempt or would a T-bill fund be exempt as well? I'm guessing non-exempt with my luck. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| No More Mr. Nice Guy |

4% is for your spendable net worth. At the end, many sell their home and rent (including senior living), so the equity becomes spendable. But until then it isn't spendable and should be cautiously considered in the plan. A reverse glide path for your mix of stocks/bonds can increase your success rate, especially when interest rates are high. I don't have access right now to my files, but we have something like 20% stocks, the remainder is bonds and money market, plus silver and a bit of gold. What kills a retirement success is losing a bunch in the first few years, so less exposure to stocks is better. Aim for 60/40 to 70/30 at around age 75. Data seems to show 60/40 to 70/30 is a sweet spot and not different from each other. So one might hit retirement with 20% stocks, 80% bonds and money market. Then rebalance the ratio each year by say 5%. The first year is 20/80, the next year is 25/75, the year after is 30/70, etc. This strategy assumes one has sufficient net worth today, and the goal is not to increase net worth until death. It is assumed one's goal is to avoid losing too much to sustain the current lifestyle. Whether you will leave a big inheritance under any strategy is a total guess, but this strategy may tend to reduce that probability but it should increase the probability of not running out of money yourself, especially if one retires into a bad stock market. Regarding bonds, I learned the hard way to avoid bond funds. They can vary in value just like any other etf or mutual fund! As the interest rates change, existing bond values change. Bonds held to maturity guarantee you no loss as long as the issuer isn't bankrupt. So, I buy T-Bills and hold them to maturity. Thus I don't care if they vary in value along the way - I get my interest and I get back my investment. | |||

|

| Powered by Social Strata | Page 1 2 3 4 5 |

| Please Wait. Your request is being processed... |

© SIGforum 2026