Go | New | Find | Notify | Tools | Reply |

Not really from Vienna |

Being a landlord is a pain in the ass. I’ve been working for months to repair and repaint my last rental house. The previous tenant had two dogs and a cat (the lease allowed one dog). The dogs chewed the front door jamb and frame and scratched a hole in the fiberglass front door, chewed on the closet doors, the cat pissed all over the place, the tenant painted the walls dark gray and orange. She did pay her rent on time (mostly) but I decided I no longer have the stomach to deal with tenants. I’ll be selling it soon as I finish the work. | |||

|

| Victim of Life's Circumstances  |

No way. The 1st million is the hardest. I did rentals for 50 years and made a pile but earned every cent. Got out 5 years ago and life is sweet. Keep doing what you're doing or use Dogs of the Dow and pick your own stocks. ________________________ God spelled backwards is dog | |||

|

Truth Seeker |

Absolutely not! If you needed $10-$15K for something then I would say yeah take a loan out of the 401K as you will pay yourself back plus the interest. I did that once to buy a good bit of silver. However, don’t cash out early; especially for a large amount like that. The more you have in the 401K, the more money you are making. Also as others have said, no way in my life would I be a landlord. I have never done it and never will. Absolutely every single person I know who rents out properties has nothing but horror stories to tell. NRA Benefactor Life Member | |||

|

| come and take it |

I did a dumb thing when I was younger and cashed out a 401k. It's not a good idea. 401k really takes very little to no time or energy. I became a landlord 16 years ago. I'm okay at it, have learned a few things although not an expert. I do think diversifying and having real estate is a great thing but it is not as easy as it looks sometimes. Let me smash that $3,200 a month figure real quick. $3,200 income - $320 property management, or do the job yourself - $160 (factor in a 5% vacancy rate) - $291 rental dwelling insurance - $313 property taxes - $650 repairs & maintenance $1,466 a month after expenses. This is a lot closer to what it will be. Yes you are talking about a new duplex and it likely won't have a lot of repairs in the beginning, but that bill will come some day, I guarantee. If you were to add a mortgage you can see how tight this gets, or it can go negative. You would really want to find a location where you can get 1% of the purchase back in rents a month. If you want cash flow for $400k invested it's best to find a location that can generate $4k a month in rents. That's very hard to find and does not exist in some states. "The left can't applaud me because their hands are in other people's pockets." - Javier Milei | |||

|

| Member |

So in 20 years you will have 1.5 million minus expenses. A S&P index fund essentially doubles every ten years. So starting with the same 1.2 million. Ten years later 2.4 million. Twenty years later 4.8 million. | |||

|

Drill Here, Drill Now |

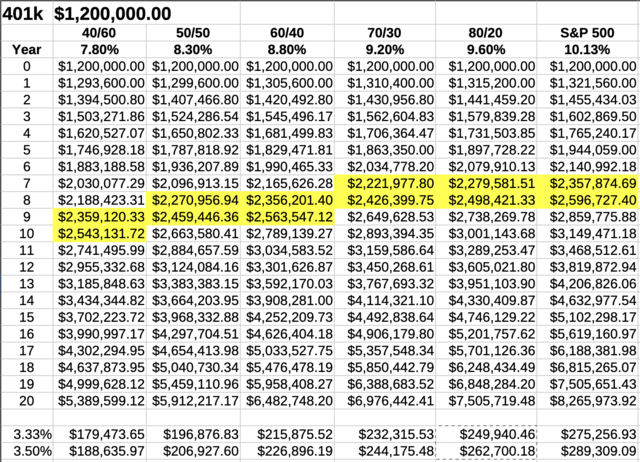

S&P 500 historically returns 10.13% so it doubles between year 7 and 8. An 80/20 portfolio historically returns 9.6% so it doubles between year 7 and 8. In 20 years, $1.2 million would be worth over $7.5 million. That's without adding more contributions to it. I think the 4% rule is bullshit in the modern inflation based economy. 3.33% to 3.5% is more realistic for retirement spending allowing you to maintain current lifestyle and have it last 30 years. For an 80/20 portfolio, that's $250k to $263k per year you can spend retirement year #1 and inflation adjust remaining years. That's a hell of a lot better than getting rental income now, and a hell of a lot less headache.  Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| Member |

The penalty for early withdraw is to steep in my opinion so a bad idea. I know a couple of guys that were into rental properties and now they're out of the rental property business due to the headaches associated with bad tenants and repairs. If you're lucky rental properties can be a cash cow but they can also end up being money pits. | |||

|

His Royal Hiney |

Finance it another way other than your 401k. You don’t need to buy the duplex outright. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

Member |

I think the better question is what will the 401k balance be in 20yrs if you just leave it alone and let it continue to grow??? It seems as though you already have a plan that is working pretty well. If you're dead set on owning a rental, my advice is to ask yourself how much time you have to invest---not how much money. Time is worth more than the cash in most cases. Secondly, compare single family properties vs the condos/townhomes. Single family=NO HOA, rent to whomever you want, rent rooms or whole place--furnish or not furnish. Condo/townhome=how much is the HOA, am I responsible for the roof, grass, siding, etc...or do I just own the inside. Rental restrictions from the city or HOA??? and on and on and on. Keep pumping $$$ in that 401k and make sure your home is paid in full asap is my suggestion. "It's gon' be some slow singing -n- flower bringing............ if my burglar alarm starts ringing" | |||

|

| Optimistic Cynic |

I would not consider this a good investment, just based on the numbers. With the figures the OP quotes, this works out to about a 9% APR return on the $400K invested. That is, if and only if there are no expenses attached. Those of us with houses know the reality of that. Not to mention potential tenant problems and vacancies. If you can borrow the money at under 6%, maybe, but the cash flow is likely to be minimal after expenses. Don't forget that there can be significant time and effort needed to manage rental properties. Your tenants are unlikely to make this easy for you. Better figure in the cost of a couple of pairs of painter's pants. But maybe you enjoy getting up at 4:00AM to unclog a toilet half way across town? Then there's taxes. Anything you make as net will be added to your regular income, perhaps even forcing you into a higher tax bracket (if you are lucky). The most significant thing you will get out of an investment like this is appreciation over time. Of course this means capital gains taxes on top of everything else. If you really want to invest in real estate, find a REIT to put (some of) your 401K dollars in. | |||

|

| I don't know man I just got here myself  |

Look into Real Estate IRA. 401K money invested stays tax deferred. Set it up as a Real Estate LLC so all expenses are deductible. Very strict rules on what you can and can do but it may make sense for you. | |||

|

| Member |

I recommend using other people's money. The government has lots of low money down programs. I would look into those. Do not cash in your 401K I have been doing Real Estate for 50 years. You can make and lose a lot of money. I have done both. Real Estate goes through boom and bust cycles. Florida is a very volatile market. I have a house there that went from $350K to $135K and now back to $400 over 18 years. You need a good real estate lawyer and accountant Being a Landlord is hard work. A lot of people get rich doing real estate. A lot of people also go broke. | |||

|

| Member |

edited sorry | |||

|

| Member |

Totally agree and I was being ultra conservative. The most accurate numbers show that it’s an even worse idea. It also keeps you from spending more than you should because you just forget about it. Getting those monthly checks will cause most people to spend a lot of it and then the numbers at retirement are even worse. | |||

|

goodheart |

I have three rental properties, because they were bought with 1031 exchanges to defer capital gains tax when we sold our residence and a vacation home. Turns out I net about 50% of the gross rental income, year after year; that's with only one loan on one property. If I had more debt than that, the net income would be way less than 50% of gross. When my wife or I die, the capital gains tax goes away, my heirs can sell the properties, and probably should. If you lose your job, the income from the rentals will very likely not cover your expenses. Then you're watching what would have been a 401k increasing in value be living expenses eating up everything, and no retirement. _________________________ “Remember, remember the fifth of November!" | |||

|

| safe & sound |

If so many people who rent/lease real estate were loosing their butts, wouldn't there be far fewer people renting/leasing real estate? | |||

|

| As Extraordinary as Everyone Else  |

I have had rental properties for over 20 years. The ONLY reason I’ve done it and made money is that I (my company) built the properties so I was getting them at a significantly reduced rate. On a slightly different note, if you are looking at setting yourself up for a better retirement consider moving a portion of your 401K into a Roth IRA a little at a time, year by year… Talk to a financial advisor to set up the best strategy for this. ------------------ Eddie Our Founding Fathers were men who understood that the right thing is not necessarily the written thing. -kkina | |||

|

Member |

Not only no, but hell no. Real estate is a nightmare. I’ve been through multiple market crashes/recoveries and I’ll take the market over landlording any day and twice on Sunday. If you were already cash flow positive and needed somewhere to park cash then (still no!) maybe… if you already knew what you were getting into. But to take a loan or cash out a tax deferred asset? Seriously, hell no. Can you contribute to a Roth? You have $1m at 41 and even conservative estimates double it every 7 years, so you’re looking at $4m easy by age 62. Way more with aggressive investing and catch up. Great job accumulating that nest egg. That is your safety net and lifeline. You’d have to take major risks to touch that with real estate in the same time period. I’d talk to a financial advisor about Roth contributions and conversions to see if they make sense now. Taxes are only ever going to go up. Minimum distributions can really bone you if you don’t need them. Really, congrats on the savings. You’re miles ahead of most people. _________________________ You do NOT have the right to never be offended. | |||

|

| Drill Here, Drill Now |

Agree Investing does have risks and there are some years you scratch your head wondering why you're invested instead of having it in a savings account. For example, this chart shows the average return as well as the best year and worst year.  The table I posted earlier is just average returns and doesn't consider risks. The chart does a better job explaining risks. However, what I really like are the tools from my advisor: Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| If you see me running try to keep up |

I can’t say either way but I will pass on some advice I got years ago from a guy who owned many properties. He said to buy a quadplex and count on 1 person not paying/being a problem so the other three will pay for the property. If you do choose to pull it out make sure you get with an accountant to get set up properly to reduce your future tax liabilities. Set it up as a business so you can properly write off everything associated with it. BTW, check out a YT channel Codie Sanchez. She seems to offer some pretty good advice on how to make money. | |||

|

| Powered by Social Strata | Page 1 2 3 |

| Please Wait. Your request is being processed... |

© SIGforum 2026