Page 1 2

Go | New | Find | Notify | Tools | Reply |

Member |

I'm still trying to learn about income and taxes in retirement, including social security. And I'd still like to find a FA I can trust to help guide me through this. One point of confusion I have for which I hope you guys can shed some light: It sounds like, if I wait until full retirement age (67), then I will get the full social security benefit I am due regardless of any other income sources (investment income, capital gains, 401k withdrawals, etc). However, it sounds like if the income, inclusive of 50% of my social security benefit, is greater than some amount (let's say $44K), then my social security income will be (federally) taxed at a rate of up 85%? Is this right? And then on top of that, a state may tax it as well (state tax rate applied to the social security benefit? or the benefit leftover after federal taxes applied?). In either case, if I have income greater than $44K (capital gains, investment, 401K, etc), then basically I will have no social security benefit, even after full retirement age. Is this correct? If so, I'm in trouble - I was assuming / counting on having that benefit. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | ||

|

| Partial dichotomy |

You still receive your SS benefit, but yes, income over that threshold a part of it will be taxed. As for waiting til your full retirement age, I'd (and did) take it sooner. There are calculations out there that show a break even point and of course it depends on your situation, but typical is 77 years old. You're betting you'll live beyond that to make waiting worth it. Since I wanted the money now when I can use it more effectively, I took mine at 64 1/2 years. On top of that, I don't trust the system to stay completely solvent. They'll have to come up with some changes. Hopefully Fed will chime in. He's the expert. SIGforum: For all your needs! Imagine our influence if every gun owner in America was an NRA member! Click the box>>> | |||

|

| Member |

It means that 85% of your SS benefit will be taxed. NOT at an 85% rate. | |||

|

| Green grass and high tides  |

That does not seem right? "Practice like you want to play in the game" | |||

|

| Member |

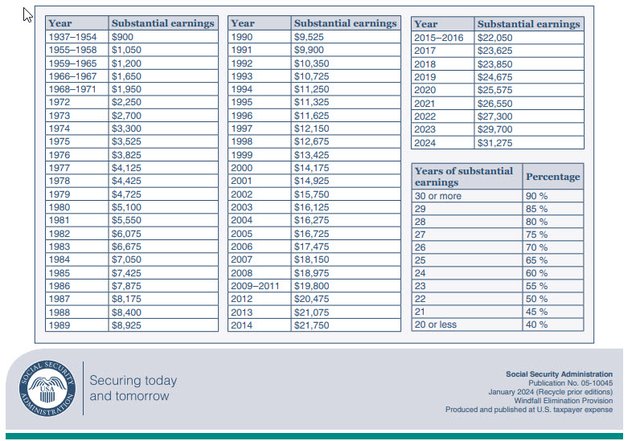

My research shows that 401K and covered pension (you paid taxes on the wages you earned from the employer) income does not reduce your SSI. A non-covered pension (if you receive a pension from a government job but did not pay Social Security taxes) can reduce your SSI by the Windfall Elimination Provision (WEP). If you have more than 30 years of taxable income and worked in a job that withheld Social Security, you are exempt from the Windfall Elimination Provision (WEP) Other income will affect your SSI. There is a table that shows the maximum deduction. Windall Elimination Provision  | |||

|

| Member |

if your comment is directed at my post, you may read about it here. https://www-origin.ssa.gov/ | |||

|

| Green grass and high tides |

No, it was in reference the op. thx "Practice like you want to play in the game" | |||

|

| Member |

Up to 85% of Social Security income is taxable for individuals with a total gross income of at least $34,000 and for couples filing jointly with a combined gross income of at least $44,000 including Social Security. Ahhhh! Need to read carefully. I think I was reading it wrong and hope you're right. Upon reading more carefully, it does sound like 85% of the benefit would be subject to taxation but doesn't specify the rate. I was alarmed with m;y initial reading - 85% of the benefit would go away as taxes. I'd guess the standard tax rates would apply based on how much income you actually have (ie - different tax rates for $50K income vs $250K income). That would make more sense. In this case, one would be guaranteed at least 15% of the benefit, and then a (majority) of the 85% of the benefit that would be subject to taxation (say at the 15% or 20% rate). Does this sound about right? If so, then not palatable but not as alarming either. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

Member |

Social Security is based on a sliding scale that is determined by the year you were born and the age when you start drawing SS payments. Create an account on the SSA website (I recommend using two factor authentication) to see your payments. There is an age at which you can collect full (100%) benefit and an age when you can collect maximum benefit (120%). That will answer part of your question, find a financial advisor for everything else. Ask friends and/or family to recommend an FA in your area. A good FA will lay out the options and you decide when start drawing Social Security. Pensions, savings, stocks and 401k play into the picture as well. This stuff isn't easy and getting advice from people who know the ins and outs, including your personal situation, make it easier to navigate. Let me help you out. Which way did you come in? | |||

|

Member |

To determine the amount on line 6b (social security) - On your form 1040, add line 2b (taxable interest), line 3b (ordinary dividends), line 4b (IRA distributions, if applicable), line 5b (pensions and annuities), line 7 (capital gain or loss) & line 8 (additional income from Schedule 1, line 10) - this assumes you have no wages or salary. Then use Worksheet 1 in IRS Publication 915 to figure your taxable benefits. Once you determine this amount, it is added into the calculation for your total income (line 9, Form 1040), which is eventually applied to your final tax calculation. _________________________________________________________________________ “A man’s treatment of a dog is no indication of the man’s nature, but his treatment of a cat is. It is the crucial test. None but the humane treat a cat well.” -- Mark Twain, 1902 | |||

|

His Royal Hiney |

I just updated my own Excel Tax Planning sheet yesterday as the picture below shows. I'm just trying to give you the confidence that I know what I speak of. I'm not saying the others on this thread don't, because I haven't looked at the other posts closely. My head is still swimming in the numbers plus I sold most of my equity positions in the face of the market jitters this morning. If you wait until full retirement age, you get your full social security benefit. Period. If you opt to get your social security when you are able to, like age 62, you get reduced benefits. If you wait after your full social security retirement age (67), you get 8% additional for each year past age 67 until it maxes out at 24% more at age 70. If before your full retirement age, you're receiving your social security benefit and are still working, they will deduct $1 from your social security benefit for every $2 you earn above the annual limit. For 2024, the limit is $22,320. If the combined income of you and your spouse is below $25,000 for the year, your social security benefits is not taxable. If your combined income is $25,000 and below $34,000, 50% of your social security benefits is taxable at your marginal tax rate. If your combined income is over $34,000, then 85% of your social security benefits is taxable. Your combined income is calculated as follows: Your Adjusted Gross Income + Tax Exempt Interest - 50% of your social security benefits. I blurred out my personal numbers for obvious reasons But what you have to do is 1. You get taxed on your ordinary income. Your Ordinary Income is your Taxable Income minus your Long-Term Capital Gains. Your Taxable Income is your Adjusted Gross Income minus either 50% or 15% of your Social Security Benefits (depending if your 50% or 85% of your SS benefits is taxable) minus your deductions (I used the standard deductions for planning purposes). Your ordinary income is taxed using the regular Income Tax tables. 2. Then you get taxed on your Long-Term Capital Gains. If your ordinary income is below $94,050 then it's zero tax. if your ordinary income is between $94,051 and $583,750, then your Long-Term Capital Gains tax rate is 15%. Over $583,750, then your gains is taxed at 20%. You add your Tax on Ordinary Income and your Long Term Capital Gains Tax and that is the total tax you have to pay to the US Federal government. As a retiree, no one takes taxes other than me so I have to pay it myself. And I calculate ahead what I expect to earn so I can figure out what I have to pay in taxes during the year. There's also a rule that you have to pay taxes as you earn but if you pay your taxes as part of making an IRA withdrawal in December, the IRS computers think you made the taxes in January of that year or so I'm told by some YouTube guy. I don't quite wait until that long. So I have to figure out how much I have to withdraw from my IRA for living expenses, and I also have to figure out how much I have to withdraw from my IRA for taxes and, on top of that, I have to figure out how much additional I have to withdraw for taxes to pay on the withdrawal I make to pay for my taxes. So if I have to withdraw $2,300 to pay for my taxes, I have to withdraw a total of $3,046 so I can have the $2,300 to pay for the tax and the remainder is for the tax on the $3,046 I just withdrew. Also, as you can see, I keep track of the IRMAA threshold where if you go over by $1, then you pay extra in Medicare premiums two years down the line. So between the IRMAA threshold and what I need to withdraw from my IRA to live on and to pay my taxes, that tells me how much I can convert into my Roth IRA account which will be tax free and available 5 years down the road. This rule is a bit more complicated because you don't know what the limit for 2024 income will be in 2026 but I use 2024's limit for 2022's income as a proxy and I'll be sure to not exceed it. If you have any more questions, feel free to email me but let me know first by tagging me in this thread as I don't really check that email address regularly.  "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

goodheart |

California does not tax Social Security income. _________________________ “Good intentions will always be pleaded for every assumption of authority. It is hardly too strong to say that the Constitution was made to guard the people against the dangers of good intentions. There are men in all ages who mean to govern well, but they mean to govern. They promise to be good masters, but they mean to be masters. –Daniel Webster (1782-1852)" | |||

|

Casuistic Thinker and Daoist |

I was happy to discover that when I started drawing SSA at age 62...break even was too far down the road for my comfort. Plus that I was able to draw survivor benefits for my daughter until she reached age 18...not taxable under Federal or State tax codes No, Daoism isn't a religion | |||

|

| His Royal Hiney |

But the Federal Government does. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

Told cops where to go for over 29 years… |

I just retired and will start collecting SS next year when I turn 62. My understanding is my state pension and personal retirement distributions while considered “income” for tax purposes are not “earnings” that impact the taxation of the SS amount. Do I have that correct? What part of "...Shall not be infringed" don't you understand???  | |||

|

| Member |

Thanks guys! Appreciate the help and knowledge. Rey: nice spreadsheet. I'd really like to understand the derivation and implication of each cell (well, some are obvious but others are unfamiliar to me). I have a lot of learning to do and time is passing quickly. I'm finding I've probably made some less than ideal decisions to date in my ignorance. I'm trying to figure out what my real situation is and how to mitigate things. Rey: I'll send you an email, perhaps over the weekend. Thanks! "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Staring back from the abyss  |

I heard today that there's talk of doing away with that. I'm not sure if it was Biden or Trump promoting it though. Doesn't really matter as long as it goes away. ________________________________________________________ It is long past time for a Convention of States. The Founding Fathers gave us this tool to fix an out of control government and we need to use it. | |||

|

| His Royal Hiney |

You're more than welcome to ask me questions about taxes and I'll answer. Understanding the derivation and implication of each cell would not be productive for you. The formulas reflect my understanding of the tax laws as they change. You first have to understand the tax laws to understand the formulas I use. It will be more difficult to understand my formulas to understand the tax laws. I also use tables from different sheets to populate the numbers such as what I expect total taxable dividends for the year based on year to date along with Assigned Names. For example, here's the formula for the Tax on Ordinary Income: "=XLOOKUP(YTD_Ordinary_Income, TableUSTaxTable[Lower Bracket],TableUSTaxTable[Base Tax],,-1)+G16*(YTD_Ordinary_Income-XLOOKUP(YTD_Ordinary_Income,TableUSTaxTable[Lower Bracket],TableUSTaxTable[Lower Bracket],,-1))" It uses the YTD_Ordinary_Income value (calculated by another formula as I described in my previous post) to search for the nearest lower value in the Lower Bracket column in the US Tax Table to return base income tax then add to that the product of the Marginal Tax Rate (in the cell above determined similarly) with the difference of the Year To Date Ordinary Income and the bottom income of that bracket. The Long Term and Short Term Capital Gains value are added up from another table in another sheet that consists of uploaded sell records from Quicken. All the values you see are either calculation formulas or formulas pulling data from other tables. The only things I manually enter are the ones marked "What If", "Data Entry," and "Enter Total Tax." I have to Enter Total Tax manually because if I try to connect it the main flow, it creates a circular reference. I think I can use Excel's optimization function but I don't like things too complicated and needing to trust Excel's internal functions to calculate things right. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| Member |

Thanks again Rey. Got it - many of the cell derivations and utility is specific to you. I guess I should have said that I'd be interested in the conceptual attributes if they may also be applicable to me even if the derivation and/or implication may be different. For example, one utility of the spreadsheet seems to be something about IRMAA (not sure what that is, need to research it) influence to Medicare premiums and Roth IRA conversion (something which I don't do and need to learn more about). The spreadsheet is eye opening to the uninitiated. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| No More Mr. Nice Guy |

1) As I've posted before, converting IRA money to a ROTH is usually a winner. One important consideration is the 5 year rule, that the ROTH has to exist for 5 years. Start the clock now even with just a small initial deposit. The decision matrix for ROTH conversion is both simple and complicated. The simple part is your current tax rate vs future tax rate, which mathematically is the only factor in final value. If you do not convert now, you save taxes now but your future withdrawals are "income" which affects other things such as Medicare, how much of your SS gets taxed, etc. You'd have to make some assumptions and plug them into a bunch of calculations. If you happen to be in an unusually high tax bracket for the current year, conversion may not make sense. If your income is stable and representative of you future lifestyle, conversion may be a good idea. 2) Typically a retiree's income in a general sense does not go down much. That is, if you currently earn $100k then you have a $100k lifestyle. In retirement you'll have a similar lifestyle and need either $100k in taxable earnings (from your 401k or your regular taxable brokerage account), or you'll need something less from non-taxable sources such as ROTH. Those are generalizations but make the point. If all your savings are in a 401k you will have to withdraw $100k to end up with the same spendable money as you have now. If all your money is in a ROTH, you only have to withdraw what you spend. The ROTH bonus is a zero taxable income, which helps save money in other areas. 3) I am a fan of taking SS at 62, which is what I did. If you don't need the money at 62, you can bank it and let it grow. Historically your investments should average at least the 8% difference that SS has per year of delay. 4) If you are unlucky and don't live to break-even (around 80 yrs old iirc), at least your heirs get something from it. If you die before starting SS, you've spent down your own savings, leaving less for your heirs. No, inheritance isn't a big financial decision point, but it can be a big emotional factor for the survivors. My wife's 1st husband died unexpectedly in his early 50's. She is still annoyed at all the taxes he paid which he never got the benefit of, nor will his children. 5) Generally, spending down your 401k or traditional IRA first in retirement rather than taking from ROTH or regular savings/brokerage accounts makes the most long term sense. Even though it is counter intuitive to be paying taxes now rather than later, the Required Minimum Distribution kicks in at age 72. It is better to have less in your 401k/IRA at that point in time. 6) A lot of the thresholds are low enough that many people will get bitten by them. Which essentially makes them not worth worrying about. Social Security income tax, IRMAA, etc. If you are close to some of the trigger points it can make a big difference if you manage the details. 7) A good FA can model all of these things and show you different options. Realize that these are based on historical data and involve lots of assumptions about the future. 8) The psychology of being retired is very different than when you have a regular paycheck. Being debt-free is huge. Sleeping well is more important than the thrill of gambling in the market. Setting up a plan and letting it run is, for me, very comforting. | |||

|

| Powered by Social Strata | Page 1 2 |

| Please Wait. Your request is being processed... |

© SIGforum 2026