Go | New | Find | Notify | Tools | Reply |

Itchy was taken |

*** OLD Thread, brought back from the grave **** I just hit 65 and my bride will be 62 in September. Our current net is 10 k-ish a month. We're not rich, but comfortable. From you retired folks with knowledge, is there a magic number?This message has been edited. Last edited by: scratchy, _________________ This space left intentionally blank. | ||

|

thin skin can't win |

Sure. It depends. You only have integrity once. - imprezaguy02 | |||

|

| Itchy was taken |

I know _________________ This space left intentionally blank. | |||

|

| Conservative in Nor Cal constantly swimming up stream  |

I don’t know your financial status. I personally have a financial advisor that set up a plan for me. She had me do a budget at the beginning and asked what was the lifestyle I wanted in retirement. I’m set until I’m 95 at this point. You would probably get better financial advice from an advisor versus your random friends on the Sigforum. ----------------------------------- Get your guns b4 the Dems take them away Sig P-229 Sig P-220 Combat | |||

|

| Green grass and high tides  |

If it is just a cash question. Taking into account only ss x 2 as income. I would say $2 mil minimum if debt free at the time. "Practice like you want to play in the game" | |||

|

| Member |

Is everything paid off in full? Is there enough in obtainable reserve to last ten months if your income goes away ? Is everyone healthy ? Safety, Situational Awareness and proficiency. Neck Ties, Hats and ammo brass, Never ,ever touch'em w/o asking first | |||

|

paradox in a box |

Different for everyone. But some assumptions the finance guys make that I disagree with will make you think you need more than you do. I doubt I’m living to 95. I don’t need $2 million in the account when I die. I won’t be living the same lifestyle at 80 as at 65. Anyhow we plan to retire at about age 60 (average age as she is older). We will take stress free jobs to make maybe 50-60k combined for about 2 years before fully retiring. We will have about 1.5 when we do this. We will have no debt. These go to eleven. | |||

|

| Member |

I’m retired federal. If we don’t get paid then we’re all screwed. Equally | |||

|

| Member |

I retired at 55. That was 14 years ago. You don't need millions. (I certainly don't have millions, or even one of them). You just need to be debt free, completely debt free, and possess the will power (or common sense) to live within your means. It does help if you live where property taxes are low, and retirement income is untaxed by the state. ____________ Pace | |||

|

Member |

Taxes depend on the state you reside in. Social Security, Pensions, 401 may be taxable in your state of residence. Here's breakdown by States... https://www.kiplinger.com/reti...-states-tax-retirees | |||

|

| No More Mr. Nice Guy |

Whatever you have is enough. More gets you more, but if you are debt free with SS coming in, you don't need a huge nest egg. | |||

|

| If you see me running try to keep up  |

Two million is not going to happen for the average person in the US, neither is one million. It depends on your situation, if you want to protect your principle and live off interest, two million would give some leeway. I told my only child that she should not expect to have any money inherited. My wife and I worked hard to get to where we are and we did not live frugal so my daughter and son in law can live it up off our efforts. I am not worried about protecting my principle so I do not need to have millions. I have two small pensions that will cover my bills so my 401k is for us to use as we see fit. I think it is more common for children to be ruined by inheriting wealth, that is my experience from what I have actually seen from those I know. I’d rather leave my daughter only property since I can see leaving a lot of money making her and my son in law less inclined to work hard. My wife and I grew up poor and we worked hard to get ahead and made it a bit too easy on my daughter. She does not know what it is like to lack anything, to go to bed hungry, to live without electricity and have two sets of clothing, wash clothes by hand etc. I wish I had made her experience that so she would know what it is like. Being poor motivated me and I struggled for over then years to finally get away from living paycheck to paycheck. If you really want to know, see a fiduciary and let them run the numbers for your situation. Look up Monte Carlo projections and do some research and you can get some better estimates by plugging in your info. | |||

|

Member |

This was a post I made back on October 24, 2023 "How much money in savings do you really need to retire?" https://sigforum.com/eve/forum...390003405#3390003405 There was a lot of good information given. The Second Amendment to the United States Constitution. A well regulated militia being necessary to the security of a free state, the right of the people to keep and bear arms shall not be infringed. As ratified by the States and authenticated by Thomas Jefferson, Secretary of State NRA Life Member | |||

|

Fighting the good fight |

There's no magic number... The number is going to vary greatly, as everyone's situation is different. Some of the factors include: -Non-savings income (Social Security, pension, rental property, etc.) -Debts (is your home paid off, etc.) -Healthcare costs (62 is too young for Medicare, and even once of age, you may need supplemental) -Cost of living (are you in a high COL/tax area, or low?) -Other monthly expenses (have you sat down and prepared a detailed budget/expenditure sheet?) -Desired lifestyle (want to travel/pursue pricey hobbies/etc?) -Legacy (do you want to leave anything for the kids, or spend most of it in your lifetime?) -Risk tolerance (are you going to be able to sleep at night if you remain invested partially in higher risk/reward options like stocks, or would you rather play it safe by going more fully into bonds/TIPS/money market/etc.) And more.

This. It's important to note that not everyone with a job title like "financial planner/financial advisor" is a fiduciary. Fiduciaries are required to act in the best interest of their client. Whereas those that aren't are more likely recommending what's best for them (in commission/incentives/etc.) | |||

|

| Member |

Not knowing your particulars (and you shouldn't reveal on a public forum anyway), as many have said, it depends. When I retired, I was really concerned if I was doing the right thing. When I met with my financial advisor, I expressed my concerns, was I really ready financially? She said "You are better prepared than 90% of my clients. The big one for us was having our mortgage paid off. I also had concerns about being able to maintain our current lifestyle. We actually have more disposable income now than when we were working. The biggest hit to our decreased income was health insurance. At one point, we were paying more in premiums than what our mortgage had been. Now on Medicare, easy-peasy. And we didn't have a million cash in the bank when we retired. It sounds to me like you are well prepared. Just take it easy the first year or so and adjust to the new income level. Make adjustments in areas you need to and enjoy life. Good luck to you and congrats on the retirement. Tony | |||

|

Drill Here, Drill Now |

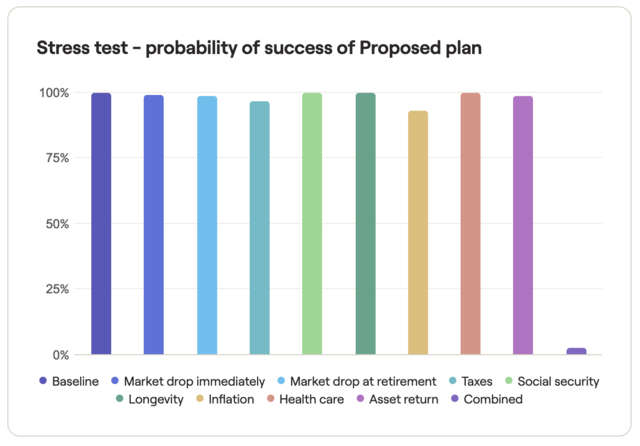

I'm 3.5 to 5.5 years from retiring. My financial advisor has done some fairly advanced modeling for me using Monte Carlo analysis. It's web based software and it includes some really nice tools where I can adjust retirement year, amount spent per month from nest egg, when social security starts, etc. Additionally, the software has 9 different stress tests such as what happens if the market drops 50% immediately after retiring or what if I live to 95 instead of 90. I'm in good shape for having enough money to last until age 90 in the baseline, and stress tests 1 thru 8 range I'm in good shape too. Stress test #9 is the ugly one which is stress tests 1 thru 8 happen all at once  I would suggest the OP hire a financial planner to do some modeling like the above as it really helps see impact of choices (e.g. which year to retire for each spouse, how much to spend per month in retirement, when to start social security, adjusting your portfolio allocation as you age, etc). Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| Green grass and high tides |

The cash amount I posted (2 million) was based on no info on a 401k, pension, retirement account or other liquid assets such as RE. So could he have plenty sure. Way less than 2 million if he has other wealth and income sources other than just ssx2. I am also assuming they are spending all the $120k and year and will be in retirement too. "Practice like you want to play in the game" | |||

|

| Itchy was taken |

Good info. We're over 2 mil, and will both collect healthy SS benefits. I do have a fiduciary working with us. I like this forum's advice pool too. Kids are all in their 30s and well launched. We have very little debt, and that will be gone when we pull the trigger. Thanks all. I think we're going to be OK _________________ This space left intentionally blank. | |||

|

| Fighting the good fight |

Sounds like you're well ahead of the curve. A commonly used quick and dirty retirement calculation (that ignores a bunch of variables but is nice and simple) is planning to withdraw 4% of your retirement savings per year. If we go with a nice round $2M saved, that'd be $80k per year. If we take that rough starting point then add in your "healthy" SS incomes, you're in good shape for your budget to meet or exceed your current ~$120k/year. Even with just a flat $2M and the average SS income of $22,884k, that'd be $125,768/year with 4% of $2M + SSx2. Plus you stated your savings exceed $2M, which is even better. That simple 4% rate is based on playing it ultra safe and planning to live mostly off just the annual returns alone of your nest egg when invested almost exclusively in safe investments. But many folks will have no problem taking a more aggressive investment approach during retirement and earning more than ~4% and/or spending their nest egg down more quickly during retirement by exceeding that ~4% rate of return and planning to leave a smaller amount (or none) for their kids. | |||

|

| Drill Here, Drill Now |

^^^ That roughly gives you 25 years of retirement (e.g. retire at 65 and live to 90), but it's 3.33% to roughly give yourself 30 years of retirement (e.g. retire at 60 and live to 90) and it's 2.87% to roughly give yourself 35 years of retirement (e.g. retire at 55 and live to 90). BTW, by roughly I mean ignoring a metric crap ton of variables (e.g. having a stock market year like 2008). Ego is the anesthesia that deadens the pain of stupidity DISCLAIMER: These are the author's own personal views and do not represent the views of the author's employer. | |||

|

| Powered by Social Strata | Page 1 2 3 4 5 |

| Please Wait. Your request is being processed... |

© SIGforum 2026