SIGforum.com  Main Page The Lounge Question Regarding Homeowners Insurance And Skyrocketing Building Materials

Main Page The Lounge Question Regarding Homeowners Insurance And Skyrocketing Building Materials

The Lounge Go | New | Find | Notify | Tools | Reply |

| Get my pies outta the oven!  |

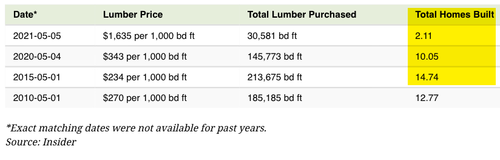

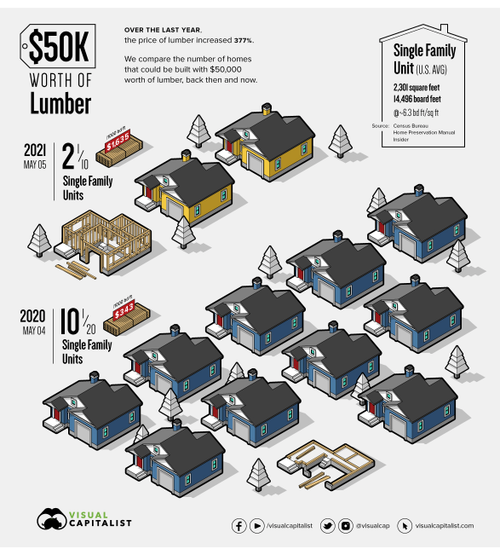

I was really shocked at this infographic today:   With $50,000 of lumber in 2015 you could build nearly 15 homes. Last year at this time you could build 10 homes. Right now you can build just TWO HOMES with $50,000 of lumber. This is making me worry about my homeowner's insurance. If my house burns down tomorrow, my current policy has a $330,000 rebuild allowance which in 2017 was more than adequate. Now? Probably not. Should I be contacting my insurance guy and having a chat or just wait until this all calms down if it ever does? My gut feeling is that this all crashes in 6-8 months or less. | ||

|

Knowing is Half the Battle |

I'm sure he'd be happy to sell you more insurance. It will also make your deductible higher if it is based on a percentage of your replacement value. In the extremely unlikely chance your house were to burn down today, that thing isn't going to be rebuilt within 6 months though. You'll be posting about it from a Holiday Inn Express for months while your claim is processed and you find a builder and then get the permits and then actually find the materials. If it was me, I'd just don't burn candles until wood gets cheaper and either donate all your ammo or send it all downrange in one magnificent weekend range orgy. Put your grill and lawnmower 100 yrds from your house. Park your cars in the street. Unplug all appliances and just eat in restaurants or get takeout. You still have your electrical, HVAC and water heater to worry about, but there's calculated risks to be made. Just kidding. I saw that same graphic and was amazed. People are scrounging in garages and snapping up used 2x4s at estate sales I've been to recently before anything else. | |||

|

quarter MOA visionary |

THAT is the scary part. Todays Biden economy vs the Trump economy. Even thought the stock market is still up for now but inflation has eaten up much of the benefits. Look at employment with no one wanting to go back to work with all of the free-shit handouts along with the Government suppression of the economy using the Pandemic as a reason. Times are scary now and confusing. | |||

|

| safe & sound |

Hypothetical related question: You experience a loss and your insurer determines and amount and issues a check. You have two years to complete the work. You never cash the check, and material prices take off. Is the insurer liable for the cost on the date of the loss, or at the time the claim check is accepted? Heck, in today's world there could be a 10% difference or more in a week's time. | |||

|

Member |

If you owned it outright that would be an interesting strategy. If there's a mortgagee clause, ie another party like a bank has interest, that wouldn't work because the mortgagee interest generally has offset to that money. The general rule for insurance in a mortgagee clause is the lesser of the loan amount vs cost of replacement. As the scales are moving, the owner could presumably end up with just a burnout lot. | |||

|

Nosce te ipsum |

I'd be dancing a traditional Zaporozhian hopak, так? | |||

|

| Knows too little about too much  |

Got my homeowners insurance bill yesterday. House value up about $45K, bill up about $350.00. Maybe some of them are paying attention. RMD TL Davis: “The Second Amendment is special, not because it protects guns, but because its violation signals a government with the intention to oppress its people…” Remember: After the first one, the rest are free. | |||

|

I Deal In Lead |

From everything I've read, there's no building material shortage, there's a transportation problem. It'll go back to normal as soon as they stop the ridiculous amounts of "unemployment" insurance people are getting and they go back to work. | |||

|

| Powered by Social Strata |

| Please Wait. Your request is being processed... |

SIGforum.com Main Page The Lounge Question Regarding Homeowners Insurance And Skyrocketing Building Materials

The Lounge © SIGforum 2026