Page 1 2

Go | New | Find | Notify | Tools | Reply |

His Royal Hiney |

I guess I missed the basic questions contained below.

If you are going to convert, you are going to convert the difference between your current income for the year that you report in your returns and one of three thresholds. These thresholds are thresholds because exceeding them increases your effective tax liability either proportionately or precipitously. The first threshold is the top limit of your current income tax bracket. Roth conversions are taxable income recognition events. If you go $1 into the next threshold, that $1 gets taxed at the higher rate. For example, if your income exceeds the 22% threshold, the amount over that threshold gets taxed at 24% and not 22%. Fortunately, this is proportional. The second threshold is the IRMAA thresholds, the lowest of these is around $218,000 (joint returns), so if you exceed this amount by even 1 dollar, adjusted for inflation two years now, you’ll be paying Medicare surcharges, the lowest is an additional $1,140 for the year for your Medicare premiums. The third threshold is new - $6,000 deduction per senior from the One Big Beautiful Bill. The maximum Modified Adjustment Gross income is $150,000 (joint) and it phases out completely at $250,000. This deduction will phase out in 2028. Just 3 years. Saving taxes on $12,000 now is a better proposition than saving taxes for age 73 and up. Converting the difference between your current income and any one of these thresholds is called efficient tax harvesting. You’re converting money from your IRA that you don’t need to meet living expenses into a Roth account. Since you don’t have post-taxed money to pay for the money, you’ll need to take the tax Money out of the difference. No. Big. Deal. Assuming you have the difference between your income and threshold; we’ll call that the gross amount. Net Conversion amount = Gross amount × (1 - marginal tax rate) If you also need to pay state taxes out of that amount, be sure to add the Fed and state marginal tax rates.

When you do Roth conversions, you reduce the balance of your tax deferred accounts. This means when you start having to take RMDs and applying the percentages of how much to take, the percentage of a lower balance means the amount you’re forced to withdraw and be taxed on is less. You already taken a portion out that you didn’t need for living expenses and put it in a Roth IRA where it can grow tax free. the amount of social security you get is determined by when you start drawing, how much your earnings have been, and CPI adjustments. Your conversions and other earnings have no impact on you SS Benefits. How much of your Social Security is taxed is affected by your other income. The taxation of Social Security benefits in the U.S. (as of 2026) is determined at the federal level by your “combined income” (also called provisional income), which is calculated as: your adjusted gross income (AGI) + nontaxable interest (like from municipal bonds) + half of your annual Social Security benefits. Up to 85% of your benefits can be subject to federal income tax depending on this figure and your filing status, but never 100%. These thresholds have not been adjusted for inflation since they were established and remain unchanged for 2026. Note that a new $6,000 senior deduction (per qualifying person age 65+ under the One Big Beautiful Bill Act) can reduce your AGI, potentially lowering or eliminating the taxable portion of benefits for some retirees.      Here’s a breakdown of the rules: Federal Taxation Thresholds • If filing as single, head of household, or qualifying widow(er): • Combined income below $25,000: None of your benefits are taxable. • Combined income between $25,000 and $34,000: Up to 50% of your benefits may be taxable (specifically, the taxable amount is the lesser of 50% of benefits or 50% of the excess over $25,000). • Combined income above $34,000: Up to 85% of your benefits may be taxable (calculated as the lesser of 85% of benefits or the sum of 85% of the excess over $34,000 plus the taxable amount from the 50% tier). • If married filing jointly: • Combined income below $32,000: None of your benefits are taxable. • Combined income between $32,000 and $44,000: Up to 50% of your benefits may be taxable (lesser of 50% of benefits or 50% of the excess over $32,000). • Combined income above $44,000: Up to 85% of your benefits may be taxable (lesser of 85% of benefits or the sum of 85% of the excess over $44,000 plus the taxable amount from the 50% tier). • If married filing separately: • If you lived with your spouse at any time during the year: Up to 85% of benefits are generally taxable, with thresholds effectively starting at $0. • If you lived apart all year: Use the single filer thresholds above. The IRS provides Worksheet 1 in Publication 915 to calculate the exact taxable amount, which is reported on Form 1040. If your benefits are taxable, they’re added to your other income and taxed at your ordinary income tax rate (not as capital gains or at a special rate).

See my answer to your first question.

As answered, a Roth conversion is a taxable income recognition event. When income is recognized, taxes are owed on that income.

Assuming you’re at least 59 1/2 years old and this is your first Roth account you’re opening, if you make a contribution any time in 2026, even in December 31, the clock starts ticking from January 1, 2026 and you can’t withdraw earnings for 5 years. Meaning on January 1, 2031, you can withdraw earnings. You can always withdraw your contributions, again, assuming you’re 59 1/2. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| No More Mr. Nice Guy |

There is one advantage to paying the taxes on a Roth conversion out of the IRA money rather than from other sources. If you withhold taxes from the money withdrawn from the IRA, it counts as being an on-time tax payment. The IRS wants taxes paid in the quarter in which you make the taxable amount. So if you take money out of your IRA in January, they expect you to file estimated taxes for the 1st quarter in April and pay taxes due then. If you don't pay taxes in April on that withdrawal you will pay a late penalty. Unless you have taxes withheld at any time during the year to cover the minimum required. So you can do a Roth conversion in January without withholding taxes, and then in December do an IRA withdrawal for the amount of taxes you will owe, and withhold 100% of it. This loophole calls it an on time tax payment with no penalty. You can use this technique for any situation where you didn't already sufficiently withhold or make estimated payments during the year. | |||

|

Member |

Wow. Thanks guys. I really appreciate the insights. It's helping me form some questions to pose to my FA. Rey: Thanks as usual for your expansive responses. I understand some of it, at least conceptually. I need to figure out how to incorporate into a detailed assessment of my situation. Some of it is new to me and it will take some time for me to digest. One aspect of this exercise to determine the extent of material impact of a conversion. I understand conceptually that I could potentially benefit (detailed assessment is still complicated but I'll try out your spreadsheet template) but not sure if it would be materially relevant. Just for concept since I don't know what the numbers will show yet. If it saves $5000 per year, that might be a marginal (indifferent benefit). But if it saves $50,000 per year, than that would be a very material benefit. In your spreadsheet template, if RMD amount exceeds my expenses, do I keep a separate column which would show that growing (post-tax) balance? Where are people putting that - just into the bank? CD? Equity/Bond investments (outside of 401k / Roth)? In any case, thanks again for your help. I've much to study so that I can pose relevant questions to my FA. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| His Royal Hiney |

You’re welcome. But you need to analyze this or anything else one facet at a time. Keep in mind what question you asked and what question my response is answering. The spreadsheet was part of the answer to the question: Will doing Roth conversions be beneficial to you. I try to give you the bare minimum answer that sufficiently answered your question because even the bare minimum is expansive enough. On the other hand, if you needed another column in order to answer the question, I would have told you to add that additional column. Let’s review the question and pick up from the spreadsheet part after you fill in the numbers. The question is: will doing Roth conversions be beneficial to you? When you get to the spreadsheet, that means you’ve passed through all the questions where the answer is yes or need more calculations. You created the spreadsheet, filled in the numbers. You like the 6% growth rate. If you don’t like it then change it to 8% if you’d like. Understand that a higher growth rate will make the numbers say doing Roth conversions will be beneficial. I would not recommend using the historical long run growth rate of the stock market of 10%. 1) because it means you’re taking the volatility of the equities market and 2) part of the growth rate is also driven by the inflation rate. Keeping it at 6% to 8% allows you to disregard inflation in all your other numbers. You can see the effect of the 6% is increasing the balance at the same time your withdrawal amount is decreasing it. If your withdrawal amount each year is 4% of the balance and your growth rate is 6%, then your tax deferred balance will be growing by 2% each year. When you’ve done the numbers for 20 years or rows, compare the withdrawal rate and the RMD rate. Let’s assume the following: your withdrawal amount (the amount you need to withdraw from your IRA to meet expenses before Roth conversions) is $25,000. The spreadsheet is for you to compare your withdrawal amount against the RMD amount and decide accordingly. For example, when you’re at age 72, your balance grows by 6% and gets reduced by $25,000; your RMD amount is zero because you’re not yet required to take a minimum distribution. At age 73, your withdrawal continues to be $25K and your RMD amount is 1/26.5 of your beginning balance. I’m just assuming that your RMD amount at age 73 is still lower than your withdrawal amount of $25,000. The RMD isn’t affecting you because you’re withdrawing more than the Required Minimum Distribution. At some point, assuming your constant withdrawal amount is less that the growth rate such that your balance continues to grow, your RMD amount is greater than your withdrawal amount of $25,000. Let’s say at a particular age, your RMD amount is $60,000 vs your withdrawal amount of $25,000. You’re being forced to withdraw $35,000 more than what you need for that year and that $35K will be taxed. Using round figures, let’s assume your marginal tax rate now is 22% and the threshold is $205,000 meaning you earn $1 more than $205k and that dollar will be taxed at the next tax rate which is 24%. Every $100 you withdraw from your IRA nets you only $76 at 24% tax rate instead of $78 at the 22% tax rate. Let’s assume that your total taxable income including your $25K withdrawal (without Roth conversions) is $200,000 a year. When you get to the year where your RMD amount is $60K, then $35,000 will be taxed at 24% instead of 22%. It’s an additional waste eaten up by taxes. So you look at those RMD amounts and using your present day numbers and present day tax tables, see what marginal tax rates will your RMD amounts push you into. Getting pushed from 22% to 24% may not be a drag but understand, IRMAA surcharges also kick in at around $205,000. That’s an additional over $1000 Medicare premium a year for each spouse. After 24%, the next rate is 32%, then 35%, then 37%. Those are pretty big drags. In that circumstance, the doing Roth conversions ahead of RMD is beneficial because you can pay at your current marginal rate using the method I provided in my answer to question 2 (selected threshold - income) instead of having to pay at the higher rate when your RMD push you into a higher tax bracket. The savings is the avoidance of the higher tax rate. Reading this answer again made me realize: the ending balance for each year must take into account the higher of the Withdrawal Amount and the RMD amount. The formula for the ending balance should be “= Beginning Balance x (1 + Growth Rate) - Max (withdrawal amount, RMD amount). This is because the growth rate must be applied to the ending / beginning balance which will be reduced by the greater amount. I hope this clears things more for you. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| Member |

Rey: Thank you. Your posts have been very helpful and I do appreciate the effort you put into them. I created the spreadsheet you suggested and some interesting things were shed. Like when RMD exceeded Expenses. And when a higher tax rate was triggered (Off hand, I think 22% to 24% is not really too material since the effective tax rate doesn't change much; 24% to 32% is more material I think). I also noticed an inflection point where the Ending Balance started to decrease (in reality, perhaps offset by savings of RMD excess less taxes). One thing I'm not sure about in this rough model is how to handle the Expense rate (Withdrawal). I have a baseline today but over time, with age, it may shift. Less discretionary spending / travel and perhaps more medical / care (ie - may need nursing care). I don't know what assumptions to make for this so in that absence, I guess just keep a constant expense rate for life? I'm still digesting the numbers and trying to figure out what they suggest. But I guess to take CONCEPTUAL, exaggerated bookends, let's say the RMD amount is $500K vs expenses of $200K. One would pay more taxes and more medicare premiums. But one could argue this person may be indifferent since "income" far exceeds expenses. Again, this is just for concept (obviously not my situation since I'm worried about this stuff). But in concept, one could be in this case and so therefore there is a line somewhere where a person goes from being indifferent to where the RMD amount is material to the long term nest egg and/or Expenses / QoL. I need more thought - but I think this gives me a better starting point for discussion w/ the FA. Again, thank you! This has been very helpful. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Shit don't mean shit |

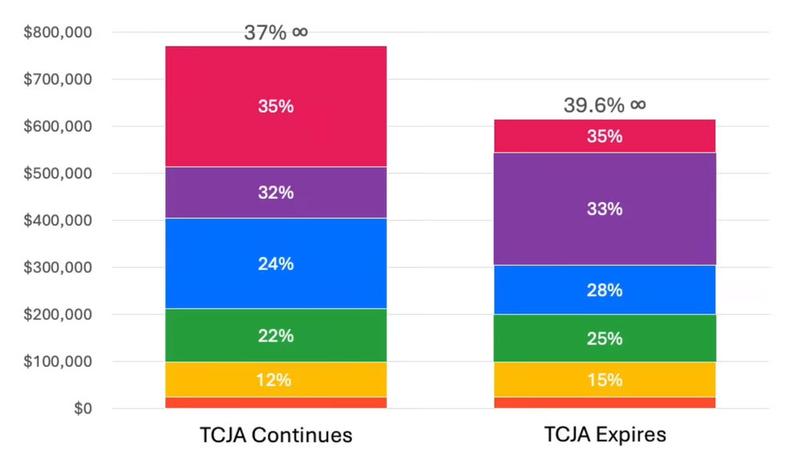

This is somewhat of a timely topic. I've been researching my options since early December as I'll be 53 this year and the vast majority of my retirement savings are in Traditional IRA / 401k. My employer does offer a Roth 401k and I have a decent amount in the Roth accounts, but I need to do Roth conversions over the next few years. I'll add a few comments / observations. Buffet has said that compounding interest is the 8th wonder of the world! As it comes to how to how to pay the taxes on the conversion, the best option is to NOT use the funds that are currently in the traditional (non-Roth) account. The reason being is you are then reducing the amount of money that is subject to compounding, which could set you back several years. In general, the younger you are the better for conversions. If you are early in retirement there may still be a benefit, but the benefit is reduced every year you get older. Not to inject politics into a non-political thread, but this is an excellent chart. Once again we can be thankful to President Trump for getting the TCJA extended permanently. Well, permanent until it is changed by and act of Congress. Nothing tax related is truly permanent. Remember this chart next time someone tells you the One Big Beautiful Bill only benefited millionaires and billionaires. TAX BRACKETS with and without the extension passed in 2025: (Particularly related to Tax Harvesting strategy)  | |||

|

| Member |

It's an interesting chart. Thanks. Aside from the tax rates, I wonder about the standard deductible and if that will be reduced moving forward. I don't really have anything wrt itemized deductions. Looks like TCJA roughly affects one's effective tax rate by a few percent (assuming an income < $300K-ish). The biggest jump is when income is > $100K (< $200K) and then > $300K (or $400K w/ TCJA). "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Shit don't mean shit |

Oh, what I forgot to mention is that chart is for married filers...because I'm married. I can't seem to find the website where I got the chart from last year. You can basically halve those numbers for single filers. | |||

|

| Member |

Hey Rey - If my 401K is 60:40 :: Equity : Bond, then should I use, say, 2/3 of 6% as the growth rate since really on 2/3 of my 401K is actually growing over time. The bond stuff is really just flat over time.... I treat it like cash with some marginal interest. I'll assume that unless you say otherwise. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| His Royal Hiney |

Yep, it sounds like you're on the right track. It gives you an big picture overview. As for truly wealthy people, most of them didn't get that way by being cavalier about taxes; a penny saved (in taxes) is a penny earned. Your retirement savings is the fuel in your tank that's going to fund the rest of your life. If you've been fortunate and diligent, your retirement savings and assets will represent the majority source of your cash flow for the rest of your life. I've always been diligent in tracking my expenses, less so my income. But, now, that I've stopped working, my monthly income is very reliable and projectable. I manage my expenses in that all in one Excel spreadsheet after exporting from Quicken. I capture all the regular expenses every month against my budget. I capture the periodic expenses that don't occur monthly. I maintain checking and minimum balance requirements for liquidity. I also capture non-periodic expenses like overseas vacations or large expenses. I also set aside an amount for reserves for whatever expense might come up. At the beginning of the year, I adjust the monthly budgeted expenses based on the last year's actuals which then is fed to a more advanced form of the spreadsheet I gave you. That's how every year, you can see if your projection still holds as the present day numbers naturally reflect inflation. For example, three years ago, our monthly number for eating out was $600; last year same frequency, same types of restaurants, the number was $1000. At least, it made my wife commit to intentionally cooking more to see if that makes a dent. But for my spreadsheet, I account for every spendable cash or asset I have and bounce that against that 20 years of yearly required withdrawals. Thankfully, the amount of current assets is more than the total of withdrawals over the 20 years by a certain percentage. I keep track of that percentage as that's also a safety factor of my plan. If it starts to go to zero, I should have a 20 year heads up unless a drastic stock market drop occurs which would affect my years 11 to 20 occurs. You should expect the inflection point where your balance starts to decrease as that's the intent of the RMD - taking out your tax-deferred savings over your lifetime and generating tax revenues for the government. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| Member |

I second triggertreat on the boglehead website and wiki articles. Those folks are helpful to the extreme and always non judgmental. "The days are stacked against what we think we are." Jim Harrison | |||

|

| Member |

Even if conversions aren’t the most efficient option, please consider the possibility of your spouse having to make RMDs with only her own deductions (you’re dead). And the possibility of paying much more for Medicare (irmaa brackets) "The days are stacked against what we think we are." Jim Harrison | |||

|

| Member |

Yes, that's a very real scenario that I need to assess once I have a good baseline to start from. I'm still refining the numbers in Rey's spreadsheet. For example, I assumed less Withdrawal once SS starts (same Expense burn rate but less 401k withdrawal needed since SS payout will cover a considerable amount). After about 5 iterations now (been doing this all morning), I think it's getting closer.... I also need to make this turnkey as simple as possible for when I'm gone. My wife is not financially savvy (I'm not either; she even less so). Very frugal though. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Partial dichotomy |

I've only scanned this thread so forgive me if this has already been mentioned, but depending on how your 401k is invested, you may want to consider rolling some or all of it into a rollover IRA. This will allow you to have almost unlimited investment options and almost certain to perform better than your 401k plan. As for a Roth...I know I'm on the same page as Fly-Sig and chellim. I'm a huge fan! I'm 67 and have been converting as much as I can tax-wise from my rollover into my Roth since I was 60. And I'll continue to until RMD time...73. Best of luck to you. SIGforum: For all your needs! Imagine our influence if every gun owner in America was an NRA member! Click the box>>> | |||

|

| Member |

Thanks again! I starting to feel more confident going into the meeting w/ the FA. And hoping he can help me dive into more details for my situation. Including an assessment of risk for the baseline (ie - I think I'm generally assuming near worst case scenario - minimal growth rate, comfortable expense rate (unless some costly health issue pops up like dementia)). Kind of you to share your expertise and methods. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| Member |

Thanks. I think once a baseline is formed, I'll tease out some concerns and/or optimization opportunities (like Roth conversion) across various scenarios (Joint, Single, Good mkt, Bad mkt, etc) and see what actions my FA recommends. Actually, I don't think he will recommend an action, he will just agree / disagree w/ my thinking. But not sure. "Wrong does not cease to be wrong because the majority share in it." L.Tolstoy "A government is just a body of people, usually, notably, ungoverned." Shepherd Book | |||

|

| His Royal Hiney |

Re: Social security. Yes, you’re starting to think in terms of cash flow. I assumed you already started taking it. I haven’t yet and my required withdrawals show that same decrease in required withdrawals as my SS kicks in. When you think in terms of cash flows, you can consider delaying Social Security past full retirement age as buying an annuity that pays you 8% for life with cost of living allowance. Of course, that means drawing down your savings but what you get for using that savings is a hard to beat 8% annuity with built in COLA protection. 5 iterations is good progress. As you begin to use it, you’ll think of things to add to help you manage either a good portion of your finances at least. My All-in-One Excel file took about a year of working periodically to improve or add the capabilities I wanted. But it was useful from the get-go. My survivor plan is this: I have a document in the bank safe that tells her how to log in to either my laptop or one of two cloud drives where in encrypted volumes, I have a master document that explains to her the contents of several files: all our accounts including what recurring charges on which credit cards. As for managing our money when I’m gone, she’s going to have to hire a money manager. But she’s capable herself since she took over in 2008 after the financial debacle and grew it nicely until I took over again after I stopped working. You do need to talk with your wife though for what to do when you’re gone. Even long before while I was still working: no big financial decisions for one year after I’m dead, don’t pay off the house mortgage, etc. Every now and then, I give her an overview of our finances so she’s informed. It will help her feel confident at least financially in case you precede her. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| His Royal Hiney |

Suggestion: I agree you should have plans of action. But, especially in the beginning, I say keep them close to your vest. Sand bag your plans, don’t even hint you have plans except maybe admit you have a ”general idea” of what you want to do. Let him come up with the suggestions and have him explain why he / she thinks it’s a good idea for you and your wife in your situation. If what he comes up matches your ideas, great! Then he can educate you on why it’s a good thing. It will confirm your thinking plus you may learn something new. If he comes up with different ideas then you can compare his explanation with your thinking. And have him justify why it’s a good idea. While you’ll find Financial Advisors with integrity and will treat their clients fairly and look out for their clients’ interests, this is still how they earn their money one way or another. You don’t have to be unpleasant or combative but you should be firm in wanting to fully understand their proposal. It’s your money after all and no one is going to care about it and your welfare more than you. "It did not really matter what we expected from life, but rather what life expected from us. We needed to stop asking about the meaning of life, and instead to think of ourselves as those who were being questioned by life – daily and hourly. Our answer must consist not in talk and meditation, but in right action and in right conduct. Life ultimately means taking the responsibility to find the right answer to its problems and to fulfill the tasks which it constantly sets for each individual." Viktor Frankl, Man's Search for Meaning, 1946. | |||

|

| Powered by Social Strata | Page 1 2 |

| Please Wait. Your request is being processed... |

© SIGforum 2026