Go | New | Find | Notify | Tools | Reply |

| Member |

Oy! I suppose I’ll be living in an RV in old age. Money manager Rob Arnott and finance professor Lisa Meulbroek have run the numbers on underfunded pension plans and come up with an interesting – and highly concerning – new angle: That they impose a “stealth mortgage” on homeowners. Here’s how the Wall Street Journal reported it today: “Real estate is the ultimate collateral for unfounded state public employee retirement obligations.” Most cities, counties and states have committed taxpayers to significant future unfunded spending. This mostly takes the form of pension and postretirement health-care obligations for public employees, a burden that averages $75,000 per household but exceeds $100,000 per household in some states. Many states protect public pensions in their constitutions, meaning they cannot be renegotiated. Future pension obligations simply must be paid, either through higher taxes or cuts to public services. Is there a way out for taxpayers in states that are deep in the red? Milton Friedman famously observed that the only thing more mobile than the wealthy is their capital. Some residents may hope that they can avoid the pension crash by decamping to a more fiscally sound state. But this escape may be illusory. State taxes are collected on four economic activities: consumption (sales tax), labor and investment (income tax) and real-estate ownership (property tax). The affluent can escape sales and income taxes by moving to a new state—but real estate stays behind. Property values must ultimately support the obligations that politicians have promised, even if those obligations aren’t properly funded, because real estate is the only source of state and local revenue that can’t pick up and move elsewhere. Whether or not unfunded obligations are paid with property taxes, it’s the property that backs the obligations in the end. When property owners choose to sell and become tax refugees, they pass along the burden to the next owner. And buyers of properties in troubled states will demand lower prices if they expect property taxes to increase. It doesn’t matter if we own or rent; landlords pass higher taxes on to tenants. Nor does it matter if properties are mortgaged to the hilt or owned outright. In time, unfunded pension obligations will be reflected in real-estate prices, if they aren’t already. A state’s unfunded liabilities are effectively a stealth mortgage on private property. Think you can pass your property on to your heirs? Only net of the unfunded pension obligations. We calculated the ratio of unfunded pension obligations relative to property values in each state. We used 3% bond-market yields as our discount rate to measure unfunded obligations, because while other assets ostensibly earn a risk premium above the bond yield, these assets can also underperform. Unfunded pension obligations range from a low of $30,000 per household of four in Tennessee to a high of $180,000 per household in Alaska. They amount to less than 11% of the average home values in Florida, Tennessee and Utah and more than 50% in Alaska, Mississippi and Ohio. There are a few surprises. California, Hawaii and New York have large unfunded obligations, but because property in these states is so expensive, the average household burden is less than 15% of the average home price. Meanwhile, West Virginia and Iowa have relatively low pension debts—but the average household obligation is more than 30% of the average home price because property is far less expensive in these states. On average nationwide, unfunded state and local pension burdens represent 20% of real-estate values. This ratio can rival or exceed an owner’s home equity, depending on the size of his mortgage. If real-estate prices adjust to reflect unfunded pension obligations, many homeowners’ equity could be at risk. As we’ve seen in Detroit, the public pension stealth mortgage can ultimately devastate the housing market. This is yet another confirmation that we’re not nearly as rich as we think we are. If your home is your biggest asset but a big part of your equity is secretly claimed by the local government, you don’t really own it. And if you’re counting on a public sector pension and home equity to finance your retirement you might be hit with a double whammy when your pension is cut (despite what the state constitution says, it will be cut one way or another) at the same time your property tax bill soars to protect what’s left of pension benefits. And the pension crisis is actually much worse than Arnott’s and Meulbroek’s research implies, because they’re using peak-of-the-cycle numbers. When the next recession brings an equities bear market, pension plans will lose money, causing their underfunding to explode. So that 20% stealth mortgage is about to get even bigger. https://www.howestreet.com/201...tgage-on-your-house/ | ||

|

Now in Florida |

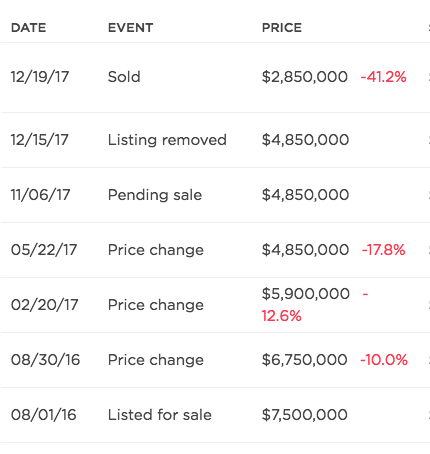

This is one of the main reasons I sold my real estate in Chicago. Eventually the bill will come due, and whoever is left there will have to pony up. Since I left, property taxes and state income taxes have risen significantly. I don't know how much more they can raise them without completely killing the local economy. I grew up on the North Shore of Chicago (think Risky Business, Ferris Bueller or any John Hughes movie) in an affluent suburb whose public schools were the envy of the nation. After a long stint in Texas, my parents moved back to that same Chicago suburb in 1996. They since put that house on the market 2 years ago and have had to drop to the price to just slightly above what they paid for it 22 years ago...still no takers. Here's the listing history for a large home in the area across the street from the lake on 3 acres of land off the golf course of an exclusive country club  It's just unimaginable. 10 years ago there would have been a bidding war on this house. This used to be one of the most desirable neighborhoods in the country for families, and now no one wants to buy there because of the current taxes and the inevitability of them going even higher. Those that are staying are renting and using their money for private schools for their kids rather than paying for the suburban life. Chicago will always be an important city due to a variety of factors - location, transportation, inertia, etc. But it is hard to imagine real growth there. The current obligations are so high, and the potential liabilities are staggering. Who in their right mind would start a business or expand there if they had any choice? | |||

|

Baroque Bloke |

The libs here in CA hate Prop 13. Serious about crackers. | |||

|

| Member |

Sounds like Kenilworth. M.I.L. has a townhouse in Lake County. It may have appriciated 50K in the last 25 years. Taxes are so high, by the time all is said and done, she'll have easily bought it twice. | |||

|

| Now in Florida |

Glencoe, but Kenilworth isn't doing much better. Everything from Evanston to Highland Park is getting crushed. | |||

|

| Powered by Social Strata |

| Please Wait. Your request is being processed... |

© SIGforum 2026