SIGforum

How is your 401k doing?

April 17, 2026, 12:33 PM

ryan81986How is your 401k doing?

My SMH is up 58% since I first bought it last year

April 18, 2026, 12:56 AM

Fly-SigWe each have our own version of diversification, with favorite funds and allocations. I think that is part of what makes it daunting to start managing one's own portfolio.

Many studies show that there are many ways to configure a portfolio that work very very well. The primary factors are: Save strongly during your working years, invest in a broad swath of the market, avoid expensive fees, let it ride through the down cycles (don't panic sell or try to time the market), and rebalance infrequently.

If one does that, the detail of which particular funds one chooses is nearly inconsequential. S&P 500 vs Russell 2000? Don't sweat it! Pick something and get it going!

April 18, 2026, 09:08 AM

6guns^^^ Time IN the market.

SIGforum: For all your needs!

Imagine our influence if every gun owner in America was an NRA member! Click the box>>>

April 22, 2026, 05:20 PM

911BossOK, I bit the bullet and have started the process of rolling over my State "Defined Contribution" account!

Just did a small ($5K) roll over amount to get the account open and figure out the process of getting it deposited to Fidelity. Finished that up yesterday and it was pretty straight forward and painless, so I initiated another disperment request today that along with the "trial" amount will equate to half of the balance in my State DC account.

Still kind of scary, but looking forward to seeing it grow faster. I will see how it goes and how the two accounts perform "side by side" for 3-4 months and then decide about rolling over the rest.

My question now is since the market is currently doing pretty good, should I buy the well performing stuff now or wait a little bit to see if there is a dip to take advantage of lower prices?

Don't want the cash to stagnate, but also would like to see some reasonably quick gains instead of buying at a peak only to stagnate in a MF/ETF and not have cash available for any deal that pops up.

Thoughts?

What part of "...Shall not be infringed" don't you understand???

April 22, 2026, 05:32 PM

6guns911Boss, we all have our threshold of risk, but for what it's worth, I rolled my company 401k over into my rollover IRA a couple of years before I even retired, because I wanted to take control of my investments. I'm glad I did.

ETA, I continued to contribute to my 401k plan until my job ended and then rolled that over too.

SIGforum: For all your needs!

Imagine our influence if every gun owner in America was an NRA member! Click the box>>>

April 22, 2026, 06:52 PM

RogueJSKquote:

Originally posted by 911Boss:

My question now is since the market is currently doing pretty good, should I buy the well performing stuff now or wait a little bit to see if there is a dip to take advantage of lower prices?

Don't want the cash to stagnate, but also would like to see some reasonably quick gains instead of buying at a peak only to stagnate in a MF/ETF and not have cash available for any deal that pops up.

Thoughts?

Invest it in what you want now.

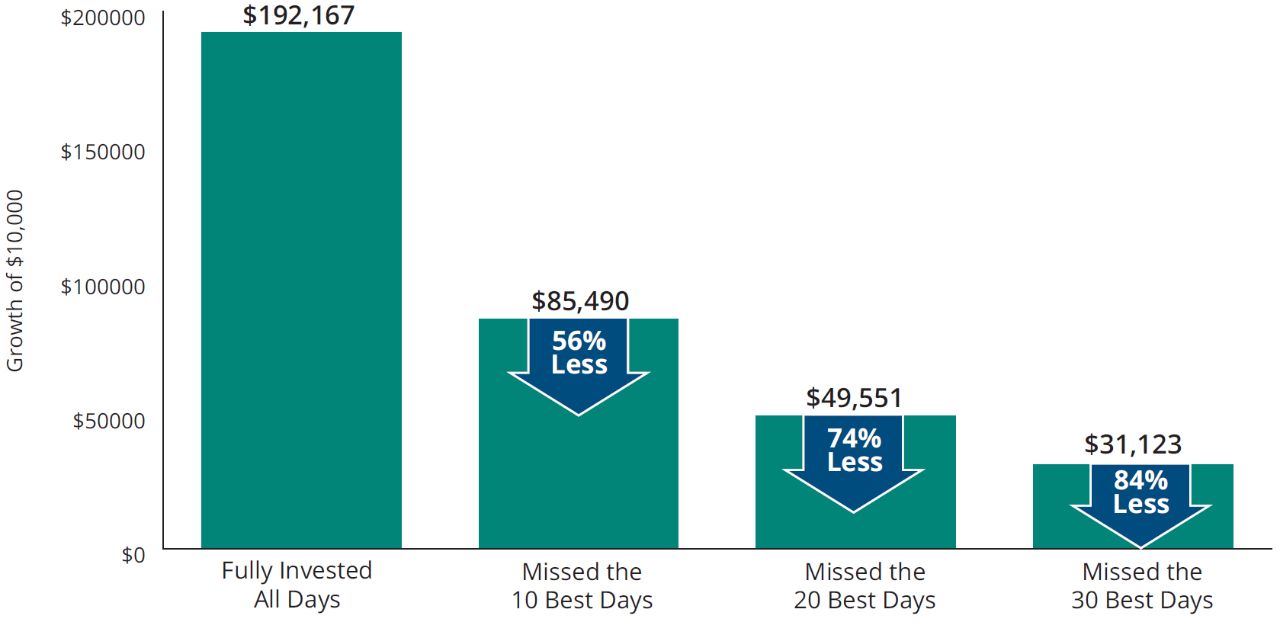

The adage is

Time in the market beats timing the market.Most of the major gains in the market are brief large spikes over short periods (often a single day) with basically no notice.

If your funds are sitting on the sidelines while you hope to recognize a good opportunity to jump in, you miss out on these, and that can make a massive difference.

For example, this chart shows how $10k invested in the S&P500 from 1996-2025 would have grown. However, if you missed the market’s 10 best days over the past 30 years, your returns would have been cut in half. And missing the best 30 days would have reduced your returns by an astonishing 84%:

Besides, it doesn't really matter what the market does today, or this week, or this month... What matters is what it does over the long run between now and when you plan to need those funds down the road.

You're investing for the long term, not day trading (gambling) to try to make a quick buck.

So invest your existing lump sum now, and then continue to roll over/add new funds on a regular basis as you go, rather than sitting around waiting for what you hope might be a better time to jump in but most likely just cutting into your returns.

April 23, 2026, 12:13 AM

911BossOk, I guess I’ll just start spending like a drunken sailor once the check hits!

Here is what I am looking at:

Symbol Name……………………………………………………1yr/3yr/5yr/10yr averages

FBGRX Fidelity Blue Chip Growth……………… 28.10% 26.52% 12.14% 19.21%

FPURX Fidelity Puritan Fund………………………15.34% 14.49% 8.35% 10.63%

FNCMX Fidelity NASDAQ Composite Index…25.55% 21.83% 11.19% 17.03%

FGRTX Fidelity Mega Cap Stock Fund…………26.86% 22.44% 15.23% 15.49%

FTBFX Fidelity Total Bond……………………………4.66% 4.61% 1.11% 2.75%

This is in addition to funds and ETF’s mentioned previously. If I can get 12-14% gains overall I will be ecstatic.

What part of "...Shall not be infringed" don't you understand??? April 23, 2026, 12:28 AM

jeffxjetSkip that bond fund, 4 percent barely/doesn't even cover inflation. Stick to the high performing stuff.

_____________________________________

"We must not allow a mine shaft gap."

April 23, 2026, 12:41 AM

911Bossquote:

Originally posted by jeffxjet:

Skip that bond fund, 4 percent barely/doesn't even cover inflation. Stick to the high performing stuff.

That was my feeling, but everything I see says “diversify”. If I get it, it would only be about 10% of my total.

The FPURX is a mix of stocks and bonds, thinking that may be the better way to still have some in bonds but a higher overall gain.

It’ll take about a week to get the rollover distribution deposited, so I have time to ponder my choices.

What part of "...Shall not be infringed" don't you understand??? April 23, 2026, 03:58 AM

Fly-Sigquote:

Originally posted by 911Boss:

My question now is since the market is currently doing pretty good, should I buy the well performing stuff now or wait a little bit to see if there is a dip to take advantage of lower prices?

Don't want the cash to stagnate, but also would like to see some reasonably quick gains instead of buying at a peak only to stagnate in a MF/ETF and not have cash available for any deal that pops up.

Thoughts?

I've been expecting a significant market downturn since 2022. There are many solid,

solid reasons. It's a good thing nobody listened to me (including myself!).

Downturns suck. They're demoralizing. They're also almost always short term, followed by a significant rise above previous levels. Any money you will need in the next 3 years should be in low risk, low volatility vehicles. Short term government bonds, money market accounts at your brokerage, or high interest CDs at a reputable bank/credit union kinds of things. Everything else should be in well diversified vehicles such as index etf's. Those longer term funds WILL see some down periods, but over time will be nicely up. Thus you balance safety and growth.

April 23, 2026, 04:04 AM

Fly-SigCheck out this chart from Vanguard. It should reduce anxieties about bear markets.

https://www.vanguard.co.uk/con...bull-chart-uk-en.pdfApril 23, 2026, 07:25 AM

chellim1^^^ The chart shows the average bear market is 9 months. That's just long enough for the weak-stomached to completely throw in the towel and bail out.

That further illustrates the psychology of a market cycle.

"Some things are apparent. Where government moves in, community retreats, civil society disintegrates and our ability to control our own destiny atrophies. The result is: families under siege; war in the streets; unapologetic expropriation of property; the precipitous decline of the rule of law; the rapid rise of corruption; the loss of civility and the triumph of deceit. The result is a debased, debauched culture which finds moral depravity entertaining and virtue contemptible."

-- Justice Janice Rogers Brown

"The United States government is the largest criminal enterprise on earth."

-rduckwor April 23, 2026, 08:13 AM

bigwagonEveryone should have a percentage of their portfolio in cash or short-term fixed assets, either to cover short-term expenses or as a source of capital to jump back into the market when everyone else is panicking and exiting. I am sitting on some huge gains in equities as a result of jumping into stocks with new money during COVID and the tariff-related market drop last April.

April 23, 2026, 08:15 AM

flesheatingvirusThe dip from the start of the shit with Iran has been completely erased. Up up up!

________________________________________

-- Fear is the mind-killer. Fear is the little-death that brings total obliteration. I will face my fear. I will permit it to pass over me and through me. And when it has gone past me I will turn the inner eye to see its path. Where the fear has gone there will be nothing. Only I will remain. --

April 23, 2026, 08:19 AM

doublesharpBuy Clorox under $100 and forget about it.

________________________

God spelled backwards is dog

April 23, 2026, 08:25 AM

bigwagonquote:

Originally posted by flesheatingvirus:

The dip from the start of the shit with Iran has been completely erased. Up up up!

Here's how at look at it when these news-cycle, panic-induced drops occur: what are the chances that the market will never reach another new high in my lifetime, or even in the next 2-3 years? Just about zero. If you are primarily a long-term buy and hold type investor, that's about as sure a bet as you can get. My only regrets are that I didn't put more new money into the market during those drops, but part of being prudent is keeping enough cash in reserve. I'm still too risk-averse to go all in!

April 23, 2026, 08:30 AM

jeffxjetquote:

Originally posted by 911Boss:

That was my feeling, but everything I see says “diversify”. If I get it, it would only be about 10% of my total.

Diversify means lots of things to lots of people, to me it means investing in a few(more than 2 but less than 10(more than that is too confusing for me)) high quality, high performing mutual funds. You can see by your own numbers that the worst performing mutual fund is 7x better than that bond fund average. Do you want to put 7x on the sideline just for someone else's idea of "diversity"?

I don't know your age, but the old thinking was as you approach retirement age you need to invest less in risky mutual funds and more in stable bond funds because:

A) most people after retirement couldn't stomach a 9-20 month downturn.

B)The age of death after retirement was on average 10 years(not sure the exact number, don't quote me on it). That meant your money barely had to cover a decade or less.

Again, I don't know your age, but if you have made it 65, barring any health issues, there is a high probability of living to 95, so your money needs to keep working for 30 years. It's a bad investment strategy to put money in a bond only earning 2.5 percent for 30 years. Inflation varies by 4-7 percent, so that money it losing buying power year after year.

Far better to keep that money working hard for you earning 10 percent plus. You just have to mentally come to terms that sometimes the market is down for long stretches of time and it will eventually come back stronger. After Trump started his kerfuffle with Iran, my 401 dropped 150K, enough to make people panic and run to bonds. I just looked at the numbers and was like "well that kinda sucks, let's see how long this will last". It lasted almost exactly 45 days or so, then came back to even, and now is like 100K up from where I started. You have to know those days are in the cards and not panic when it dips. And to paraphrase someone, "the best time to invest was yesterday, the next best time is today. Get your money into the machine as fast as possible and enjoy the roller coaster. You don't want to miss out on any gains in the next year and be like "I wish I would have put in when I first started thinking about it."

_____________________________________

"We must not allow a mine shaft gap."

April 23, 2026, 08:39 AM

bigwagonThere are other ways to invest a portion of your portfolio in lower risk fixed income securities than just a generic bond fund. A TIPS ladder, for example, is a popular way to build a low-risk, inflation-protected income stream in retirement.

April 23, 2026, 09:12 AM

doublesharpjust added some more ConAgra at $14.40. Paying near 10% div.

________________________

God spelled backwards is dog

April 23, 2026, 09:26 AM

mrvmaxquote:

Originally posted by Fly-Sig:

quote:

Originally posted by 911Boss:

My question now is since the market is currently doing pretty good, should I buy the well performing stuff now or wait a little bit to see if there is a dip to take advantage of lower prices?

Don't want the cash to stagnate, but also would like to see some reasonably quick gains instead of buying at a peak only to stagnate in a MF/ETF and not have cash available for any deal that pops up.

Thoughts?

I've been expecting a significant market downturn since 2022. There are many solid,

solid reasons. It's a good thing nobody listened to me (including myself!).

Downturns suck. They're demoralizing. They're also almost always short term, followed by a significant rise above previous levels. Any money you will need in the next 3 years should be in low risk, low volatility vehicles. Short term government bonds, money market accounts at your brokerage, or high interest CDs at a reputable bank/credit union kinds of things. Everything else should be in well diversified vehicles such as index etf's. Those longer term funds WILL see some down periods, but over time will be nicely up. Thus you balance safety and growth.

You and many others have been calling for a downturn and I think it is coming but if I could tell when, I’d be a billionaire by now.

Most people are not affected long term by drops in the market. But I do know someone whose entire retirement was devastated in the 2008 drop. He was fully in the market and lost a lot and could never recover (actually, I think he has passed away now). He had to keep withdrawing to live off and could not allow it to recover so his account kept dropping and changed his entire retirement.

So there are some people who cannot recover from the big dips. Everyone else can just get used to market fluctuations.